Full Report

The numbers behind GoDaddy Inc.: as-reported financial statements and company metrics for FY2021–FY2025, traced to the source filings, opened with the share-price history those statements have to justify. Every linked figure opens the exact page of the filing it was printed on, with the statement row highlighted. Amounts in US$ millions unless noted.

Reading notes: Display units are US$ millions (weighted-average share counts are in thousands), per the filings' own units line: '(In millions, except shares in thousands and per share amounts)'. Revenue breakdown uses GoDaddy's 'revenue by major product type' cut (Applications and commerce; Core platform: domains; Core platform: other). FY2023-FY2025 are from the FY2025 Form 10-K (Note 2); FY2021-FY2022 are from the FY2022 Form 10-K, which recast those years into the same A C/Core structure adopted in 2023. The FY2021 Form 10-K itself still used the legacy Domains / Hosting and presence / Business applications categories. Segment EBITDA is GoDaddy's reported segment-profit measure (revenue less other segment items, excluding D A, net interest, taxes, equity-based compensation, and certain other items). Income statement 'Net income attributable to GoDaddy Inc.' is shown; the FY2021-FY2023 statements also carry small non-controlling interests. 'Total stockholders' equity (deficit)' likewise shows the amount attributable to GoDaddy Inc. (NCI of $1.5M/$2.5M/nil in FY2021/FY2022/FY2023 excluded); FY2024-FY2025 have no NCI.

Share Price — Full Available History — 11 Years

The stock closed at $88.92 on Jul 10, 2026 — up 345% over the window shown (+14.1% a year), trading between $20.00 and $214.35. At that close the stock trades at 14× FY2025 diluted EPS as reported below.

Source: market price feed, weekly closes, sampled from 2,836 source observations, Mar 2015–Jul 2026. Price return only, excludes dividends.

FY2025 at a Glance

Revenue (US$ millions)

Operating income (US$ millions)

Net income (US$ millions)

Diluted EPS

Source: FY2025 consolidated statements [1] [2] [3] [4]. Click any linked figure to open the filing page with the row highlighted.

Revenue by Major Product Type

| Revenue by Major Product Type | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Applications and commerce | 1,128 | 1,280 | 1,430 | 1,653 | 1,889 |

| Core platform: domains | 1,816 | 1,959 | 2,018 | 2,153 | 2,310 |

| Core platform: other | 872 | 852 | 805 | 768 | 752 |

| Total revenue | 3,816 | 4,091 | 4,254 | 4,573 | 4,951 |

| Total revenue growth, derived | — | +7.2% | +4.0% | +7.5% | +8.3% |

Source: Form 10-K Note 2, Disaggregated Revenue (revenue by major product type) [5] [6]. Click any linked figure to open the filing page with the row highlighted.

Segment EBITDA

| Segment EBITDA | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Applications and Commerce (A C) Segment EBITDA | 448 | 523 | 594 | 739 | 857 |

| Core Segment EBITDA | 680 | 784 | 816 | 932 | 1,010 |

| Total Segment EBITDA | 1,127 | 1,306 | 1,411 | 1,671 | 1,867 |

Source: Form 10-K Note, Segment Information (Segment EBITDA by reportable segment) [7] [8]. Click any linked figure to open the filing page with the row highlighted.

Income Statement

Source: Consolidated Statements of Operations (in millions) [1] [2] [3] [4]. Click any linked figure to open the filing page with the row highlighted.

Columns marked E are consensus analyst estimates shown alongside reported results for direct comparison; they are not company guidance.

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-13. Estimate figures link to the consensus source, not to filing pages.

Balance Sheet

Source: Consolidated Balance Sheets (in millions) [9] [10] [11] [12]. Click any linked figure to open the filing page with the row highlighted.

Cash Flow

Source: Consolidated Statements of Cash Flows (in millions) [13] [14] [15] [16]. Click any linked figure to open the filing page with the row highlighted.

Long-Term Record

| Fiscal year | Total revenue | Operating income | Net income attributable to GoDaddy Inc. | Diluted earnings per share | Operating cash flow |

|---|---|---|---|---|---|

| FY2016 | 1,848 | 50 | (16) | — | 386 |

| FY2017 | 2,232 | 67 | 136 | — | 476 |

| FY2018 | 2,660 | 150 | 77 | — | 560 |

| FY2019 | 2,988 | 203 | 137 | 0.76 | 723 |

| FY2020 | 3,317 | 272 | (495) | (2.94) | 765 |

| FY2021 | 3,816 | 382 | 242 | 1.42 | 829 |

| FY2022 | 4,091 | 499 | 352 | 2.19 | 980 |

| FY2023 | 4,254 | 547 | 1,375 | 9.08 | 1,048 |

| FY2024 | 4,573 | 894 | 937 | 6.45 | 1,288 |

| FY2025 | 4,951 | 1,127 | 875 | 6.22 | 1,599 |

Source: consolidated statements across filings; older years from the standardized feed [13] [1] [14] [2]. Click any linked figure to open the filing page with the row highlighted.

Operating KPIs

| KPI | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Total customers | 20,701,000 | 20,897,000 | 21,026,000 | 20,511,000 | 20,422,000 |

| Annualized recurring revenue | 3,434 | 3,570 | 3,729 | 4,043 | 4,336 |

| Total bookings | 4,232 | 4,414 | 4,603 | 5,039 | 5,400 |

| Average revenue per user (ARPU, US$) | 187 | 197 | 203 | 220 | 242 |

| Domains under management | 84,400,000 | 83,857,000 | 83,554,000 | 81,013,000 | 80,793,000 |

Source: company-reported operating metrics [17]. Click any linked figure to open the filing page with the row highlighted.

Analyst Consensus

Current price

Mean target

Median target

High target

Low target

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-13. Estimate figures link to the consensus source, not to filing pages.

Traceability

290 of 322 figures on this page (90%) link to the filing page where they are printed — click a linked figure to open the source PDF at that page with the row highlighted. Unlinked figures come from standardized data feeds or pre-filing years.

Display units are US$ millions (weighted-average share counts are in thousands), per the filings' own units line: '(In millions, except shares in thousands and per share amounts)'.

Revenue breakdown uses GoDaddy's 'revenue by major product type' cut (Applications and commerce; Core platform: domains; Core platform: other). FY2023-FY2025 are from the FY2025 Form 10-K (Note 2); FY2021-FY2022 are from the FY2022 Form 10-K, which recast those years into the same A C/Core structure adopted in 2023. The FY2021 Form 10-K itself still used the legacy Domains / Hosting and presence / Business applications categories.

Segment EBITDA is GoDaddy's reported segment-profit measure (revenue less other segment items, excluding D A, net interest, taxes, equity-based compensation, and certain other items).

Income statement 'Net income attributable to GoDaddy Inc.' is shown; the FY2021-FY2023 statements also carry small non-controlling interests. 'Total stockholders' equity (deficit)' likewise shows the amount attributable to GoDaddy Inc. (NCI of $1.5M/$2.5M/nil in FY2021/FY2022/FY2023 excluded); FY2024-FY2025 have no NCI.

FY2023 net income of $1,374.8M was inflated by a $971.8M income-tax benefit from the release of a deferred-tax valuation allowance; pre-tax income that year was $403.8M.

FY2016-FY2018 diluted EPS is left blank (not printed in the corpus filings, which span FY2021-FY2025 plus comparative columns back to FY2019).

FY2016-FY2020 long-term figures are from the standardized data feed (SEC XBRL) and are shown without page links; the corpus contains no filing older than the FY2021 Form 10-K.

Quarterly cash-flow single quarters are derived from printed year-to-date statements (see the cash-flow note); the data feed's quarterly cash-flow series does not extend to FY2025, so no feed cross-check was available for those derived cells — each reconciles exactly to the two printed year-to-date figures.

The standardized data feed reconciles to the filings within rounding across revenue, operating income, net income, cash flow, capex and equity; no material discrepancies were found.

GoDaddy Inc.'s management explains the business in its own materials. The slides below do the most of that work, pulled from the documents preserved in Sources. Each source link opens the complete presentation at that slide in a new tab.

2024 Investor Day — 2024

Management's fullest statement of strategy, business model, segments, unit economics and financial targets — the best zero-to-understanding starting point. · Open the full document →

Q1 2026 Earnings Results — Q1 2026

The current picture: how the AI/agentic transformation is being framed today, plus the latest segment mix, margins, cash flow and capital returns. · Open the full document →

More from management

Q3 2025 Earnings Results — Q3 2025 · 38 pages · The fullest articulation of the 'Agentic Open Internet' strategy — .ai domains, AI vibe-coding and the Agent Name Service registry. · Open →

Q4 2025 / Full-Year Earnings Results — Q4 2025 · 41 pages · Full-year 2025 results and the initial 2026 outlook and guidance that this year's quarters are measured against. · Open →

GoDaddy Inc.'s management answers for the business every quarter. These are the exchanges that explain it best — verbatim, from the call transcripts preserved in Sources. Each link opens the full transcript at that page in a new tab.

Q1 2026 Earnings Call — April 30, 2026

The most recent call: Airo AI Builder monetizing within weeks of beta, Agent Name Service pitched as a new domain-like identity layer for AI agents, and buybacks defended against a rising cash balance. · Open the full transcript →

Airo AI Builder hit a $10M+ annualized bookings run rate within weeks of beta, monetizing through subscriptions plus usage credits.

Aman Bhutani, CEO: This new Airo AI Builder product offering has rapidly scaled to $10 million plus in annualized bookings run rate within weeks of its beta launch. While still early, the pace of adoption and quality of customer interaction is strong. Customers are building, publishing and purchasing incremental credits as they deepen their use of the product.

p. 2 · Read in context →

ANS a quarter on: partnerships signed and non-GoDaddy agents 'in the thousands' — early proof domains can extend into an agentic web.

Aman Bhutani, CEO: The second component of our AI transformation is Agent Name Service or ANS. We are working with large players and seeing continued interest in this technology. ANS extends the role of domains as a digital identity provider in an Agentic Open Web. We signed a couple of partnerships over the last quarter with real-world use cases and are working hard on aligning key players on the open standard and the use of Domain Name Service or DNS for agent identity and discovery. Championing the open standard and partnerships are key to getting to critical mass of support of the open standard and we are encouraged by early results. Non-GoDaddy agents in GoDaddy's ANS implementation now number in the thousands.

p. 2 · Read in context →

The monetization engine: high-intent acquisition, pruning low-value products, and Airo cohorts attaching a second product 30% faster.

Mark McCaffrey, CFO: Our focus on attracting and growing high-intent customers combined with conversion improvements is driving durable growth and higher customer quality. We are driving increased conversion into primary domains and higher attach through Airo. At the same time, we continue to deliberately manage our product portfolio, exiting lower-value offerings and reallocating resources towards higher value opportunities. And our newer Airo cohorts are demonstrating that higher value with second product attach accelerating 30% faster relative to non-Airo cohorts.

p. 3 · Read in context →

Capital-allocation policy, quantified: over 95% of free cash flow returned through buybacks across the last four years.

Mark McCaffrey, CFO: On capital allocation. We operate within a disciplined, return-based framework and have deployed greater than 95% of our free cash flow over the last four years towards share repurchases. Our continued commitment to returning capital is a clear expression of confidence and the strength of our cash flow and the long-term value we are creating.

p. 4 · Read in context →

Pressed on light Q1 buybacks with cash at a multi-year high — management says judge the track record, not any single quarter.

Trevor Young (Barclays); Mark McCaffrey, CFO: buybacks here in Q1 were well below free cash flow generation and the 95% payout stat that you've given. Meanwhile, cash at kind of the highest level since mid‑2021, if I'm not mistaken. Just any updated thoughts on capital allocation and buyback appetite with the stock at current levels? And in lieu of buybacks, any updated thoughts on M&A? […] On capital allocation, don't look at any particular quarter; look at our history — it's a good indicator of how we approach this. We look quarter by quarter, make determinations, and buybacks remain a strong lever to return value to shareholders. Our track record of returning capital shows how we approach this, and our philosophy hasn't changed.

p. 6 · Read in context →

Q4 2025 Earnings Call — February 24, 2026

The full-year 2025 call and the AI-strategy reset: a deliberate .com promo that dented near-term bookings to widen the funnel, the moat case for a 30-year data advantage, and the discipline holding margins as AI spend rises. · Open the full transcript →

The year's big bet and its bill: a .com promo to widen the funnel drew more demand than expected, cutting near-term bookings and revenue.

Aman Bhutani, CEO: We activated our marketing channels on the streamlined experience and introduced a promotional price for .com domains with a one-year term. The approach successfully increased new customer volume that purchased domain units with one-year terms. But the demand for this offer was greater than we expected. And the shift in term mix, combined with the promotional price, reduced upfront bookings and nearterm revenue.

p. 2 · Read in context →

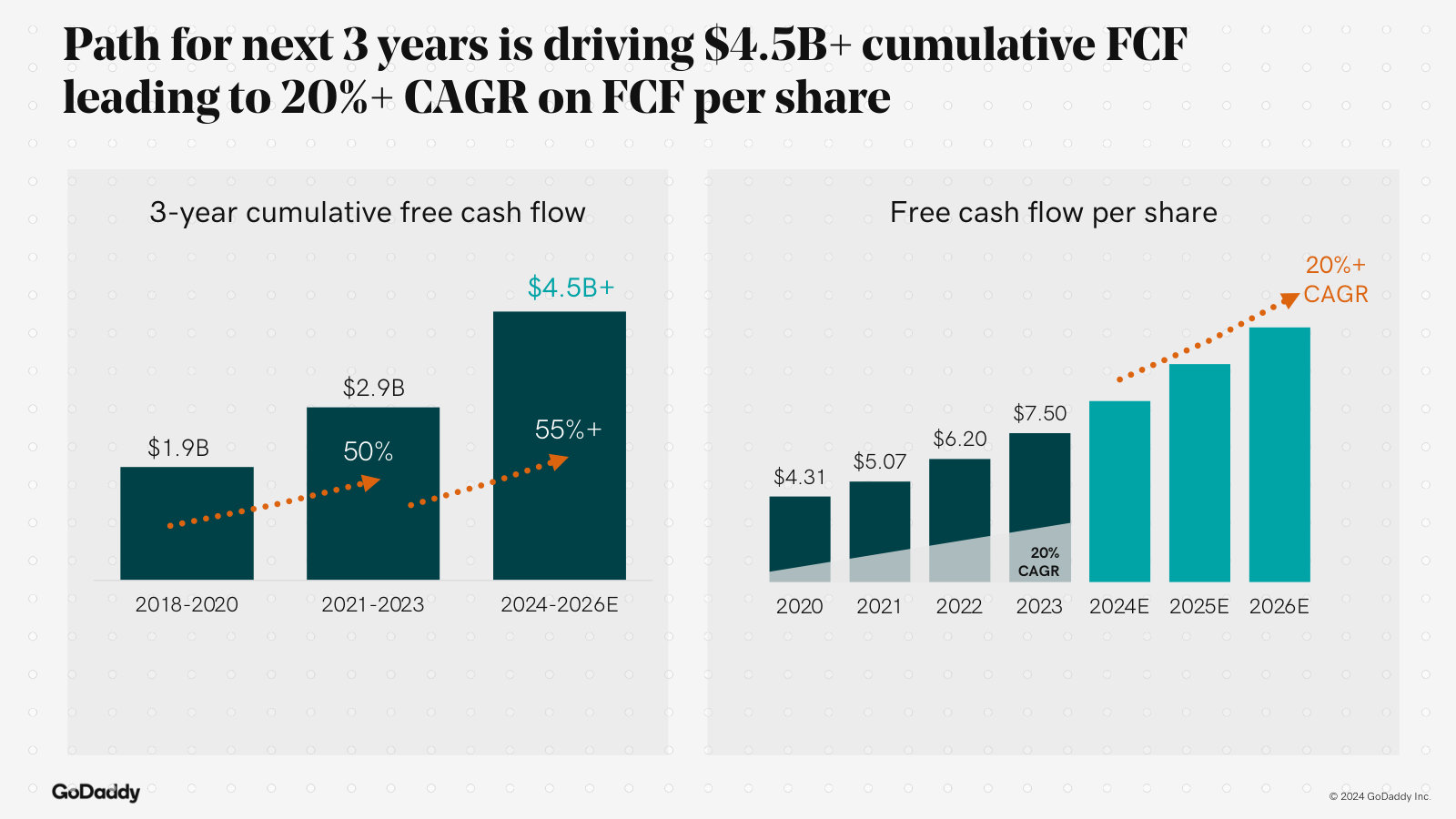

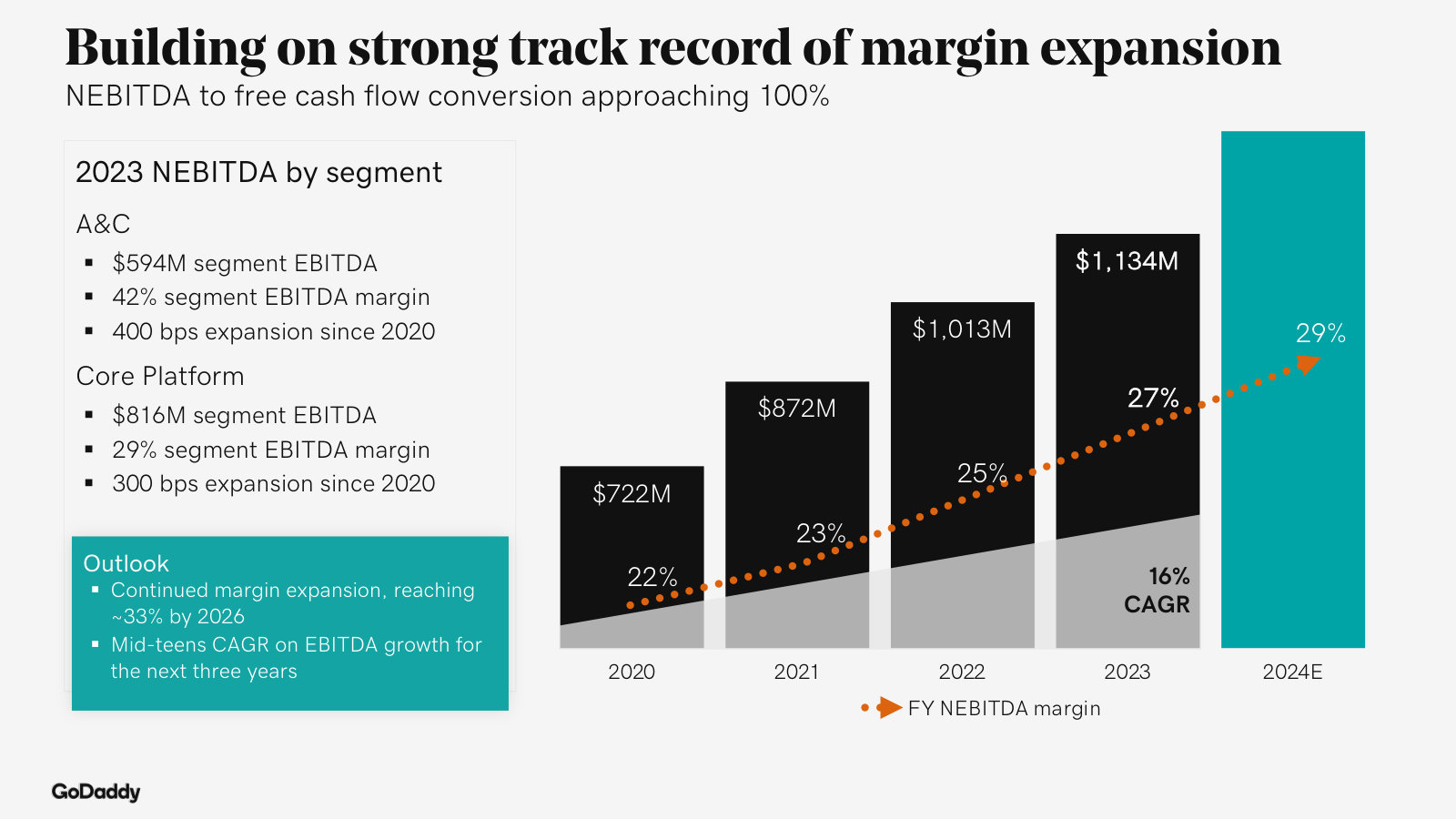

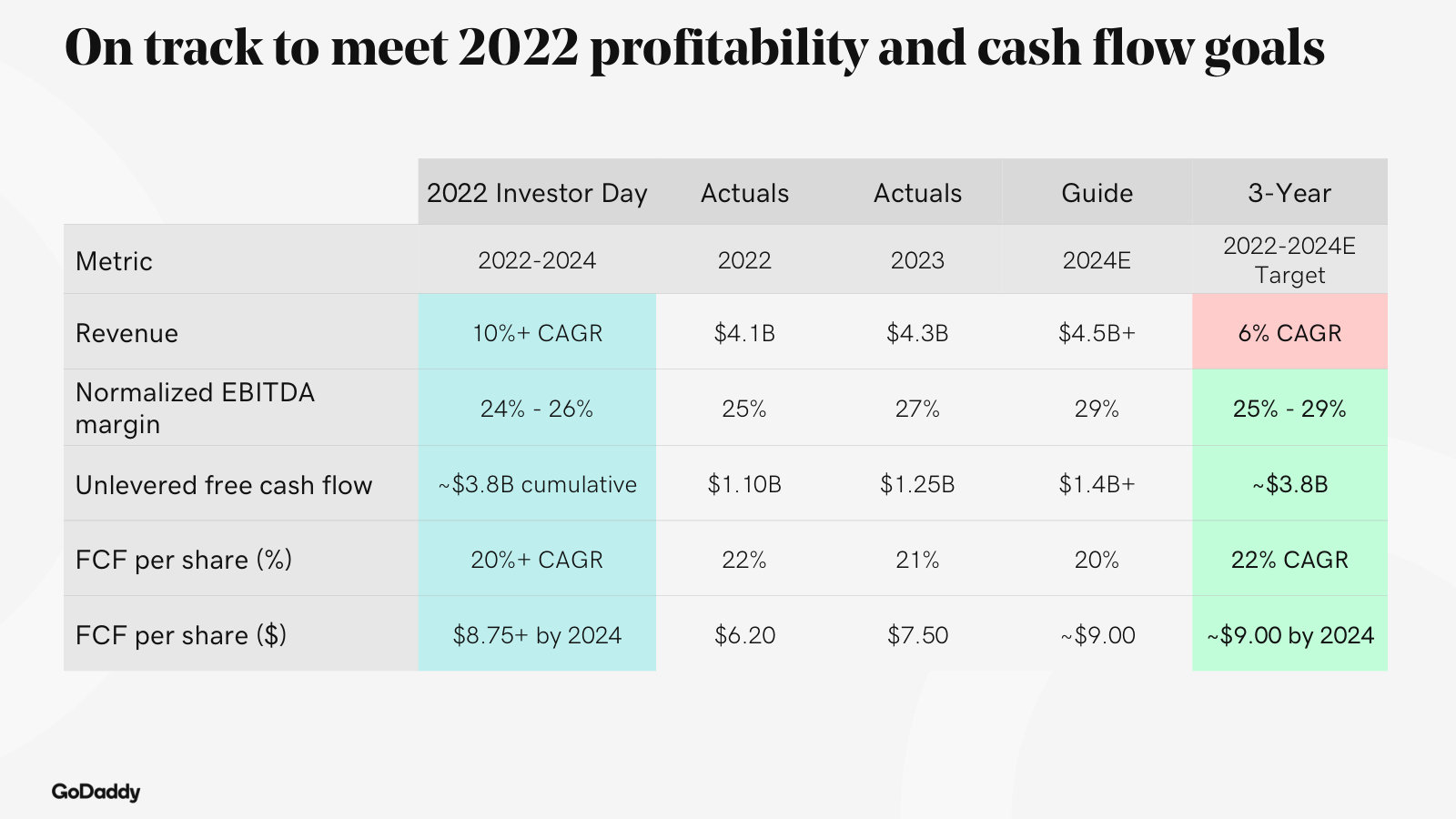

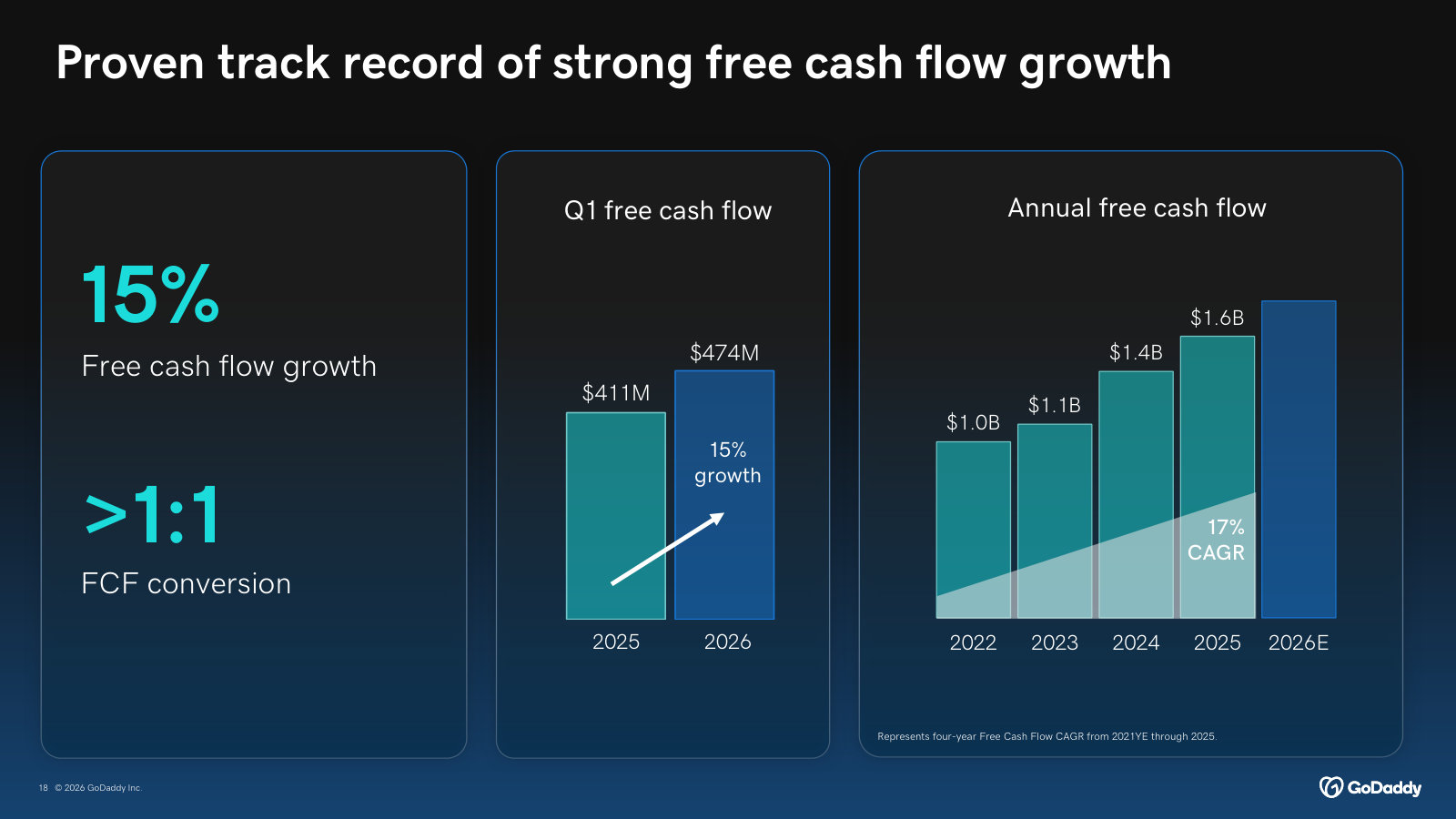

The structural story in numbers: ~1,000 bps of margin expansion over five years converting better than 1:1 into 19% free-cash-flow growth.

Mark McCaffrey, CFO: Full year normalized EBITDA grew 14% to $1.6 billion and a margin of 32%, representing 150 basis points of expansion over the prior year. Over the past five years, cumulative margin expansion of 1,000 basis points reflects our ability to scale efficiently while continuing to invest in the business. This margin expansion flows through directly to cash generation. Free cash flow grew a robust 19% to $1.6 billion with a normalized EBITDA to free cash flow conversion of greater than 1:1.

p. 4 · Read in context →

How margins hold as AI spend rises: all AI costs run through one interface for visibility, and products built to a customer-viable cost.

Aman Bhutani, CEO: One, all the AI costs go through one interface so that we are able to stay on top of it very, very closely. It doesn't matter if that's a developer. It doesn't matter if it's one of the products that our customers are using. And two, we are very focused on solving for the objective function where we create products that are at a cost that works for our customers. So what you'll continually see in our products is an already optimized AI solution that then leads to lower costs than what you might see at some other companies.

p. 6 · Read in context →

The moat vs. AI-native entrants: brand, the domains funnel, and nearly 2 billion daily data points to tune agents to each customer.

Aman Bhutani, CEO: Our competitive advantages, of course, start with our brand. It starts with our domains funnel, the scale of our platform, and the data we have about interaction with our customers, whether it's like 1.7 billion, almost 2 billion data points selected on a daily basis, all the way from interaction on the site to customers calling and chat transcripts and all of that. And we have that data globally.

p. 9 · Read in context →

On 'vibe coding' rivals: they mostly chase enterprise users, not GoDaddy's micro-businesses — 'not immune,' but little funnel impact yet.

Arjun Bhatia (William Blair); Aman Bhutani, CEO: just as you looked at your old funnel, was there anything that sort of was indicating that the competitive intensity was increasing, especially from some of the Vibe coding players out there. And Aman, I think you touched on the moat there a little bit, but I'm curious how the new motion will maybe help you sort of defend against some of the competitors that are coming into the space? […] When I look at the competitors in the AI space, we still continue to see a lot of that focus being on enterprise employees, like product managers, people that work within enterprises or people that are a little bit sort of working for agencies or companies like that. We see less of that behavior with our direct customer, the person who is the roofer, the cleaner, some micro business owner. So we see less of that. Our expansion of go-to-market is really about being able to bring more high-intent customers into the domains funnel, which is our largest funnel and then attach to it very well. Like that is the primary motion at our company, and we want to continue to reinforce that more and more. I'm not suggesting that we are immune to what's happening in the world, we just have not seen a very large impact of that in our funnel yet or at this time.

p. 10 · Read in context →

Q3 2025 Earnings Call — October 30, 2025

The landmark agentic-pivot call: Agent Name Service launched as an identity layer for AI agents, Airo.ai and 'vibe coding' builders unveiled, and the clearest statement of the domain registrar's 'right to win.' · Open the full transcript →

Agent Name Service launched: verifiable identities for AI agents, built on DNS as an open standard — staking the agentic-identity claim.

Aman Bhutani, CEO: Working back from that vision, we launched GoDaddy's Agent Name Service or ANS. Built on DNS infrastructure and proposed as an open standard. GoDaddy's ANS provides verifiable identities for AI agents. By registering agents with ANS, value is immediately created for publishers by providing their agents with a verifiable identity. Value is also created for consumers of ANS since they can securely discover and validate agents across the open web. While many companies are beginning to explore this idea, we are excited to be leading the way.

p. 2 · Read in context →

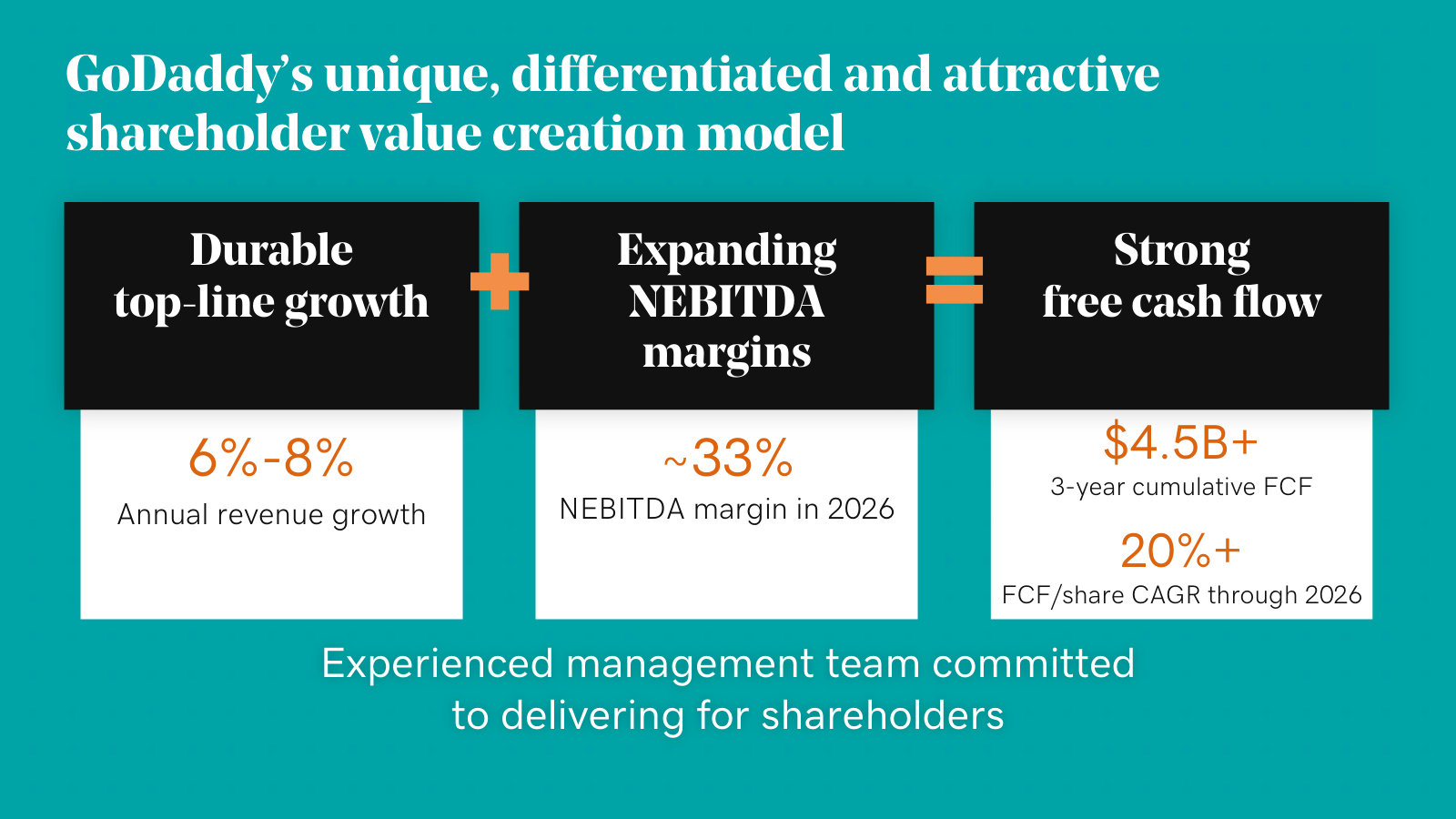

The North Star and its engine: on track to beat a 20% FCF CAGR, powered by a $500+ high-retention cohort now ~10% of the base, ARPU +10%.

Mark McCaffrey, CFO: Taken together, we are on track to exceed our Investor Day North Star commitment of a 20% CAGR. How are we getting there? As Aman mentioned, our strategy that elevates GoDaddy Airo as our primary customer engagement engine is hitting its stride. High-intent customers are adopting more products, spending more and generating higher lifetime value. Our $500-plus customer cohort now represents approximately 10% of our base, and this cohort has higher attach and near perfect retention, boosting our ARPU up 10% to $237.

p. 3 · Read in context →

How work changes: 3–5-person teams ship with ~90% AI-written code — the bottleneck shifts from writing code to everything around it.

Aman Bhutani, CEO: Now what we're seeing is teams of 3 to 5 that are using AI in the new products, 90% of the code ultimately is being written by AI. So the inefficiencies are really less and less in writing the code part and it's everything else around it.

p. 6 · Read in context →

Its right to win, by analogy to SSL: the domain start-point plus certificate-authority role make DNS-anchored ANS its claim on agent trust.

Ken Wong (Oppenheimer); Aman Bhutani, CEO: We think back to the past, it was clear you guys had a right to win in SSL, given that the website journey starts with the domain, starts with GoDaddy. Help us understand what the rationale might be for why GoDaddy can serve a similar purpose in the Agentic Internet? […] If we look back to the advent of the Internet, the solution to the identity issue wasn't just websites; it was domains and DNS that initially addressed it. Agents need to be registered so that different companies, domains, or systems can trust and verify the claims made by these agents. This is the role of the Agent Name Service. By linking it to the DNS infrastructure, one of the fundamental building blocks of the Internet, we are leveraging the core principles of how the Internet functions. The Agent Name Service goes beyond just registration; it can embed certificates, and since GoDaddy is also a certificate authority, these certificates are integrated.

p. 7 · Read in context →

Q3 2024 Earnings Call — October 30, 2024

Airo moves from promise to proof — the paywall mechanic and 40% of new website subscriptions originating in Airo — plus the clearest explanation of how pricing-and-bundling actually works. · Open the full transcript →

Airo's first hard proof: ~3M customers reached, over half engaged, and 40%+ of new Websites + Marketing subscriptions now originate in Airo.

Aman Bhutani, CEO: Nearly 3 million customers have discovered Airo with over half of them engaging with the experience. We are pleased with the momentum in discovery and engagement, and just as exciting are the proof points we are driving in Airo monetization. With many months of data, we can clearly see that the largest engagement winner is website building. Over half of engaged users published a coming soon page, which is a customizable one-page website. Customers engaged with Airo are quickly becoming the largest funnel for websites plus marketing; with over 40% of websites plus marketing paid subscriptions in Q3 originating with the Airo experience.

p. 2 · Read in context →

How pricing works: test price points to map the elasticity curve, pick cohorts balancing churn vs. upside — now reaching Core Platform.

Aman Bhutani, CEO: The way we do this is by experimenting at different price points to find the price elasticity curve. What that curve helps us do is find the right cohorts where we can balance attrition for customers, right, or let's say, retention of customers with the pricing opportunity in front of us. […] So what I'm really talking about here is that we have identified other cohorts of customers that we will be applying this approach to. Some of those are going to have products that sit in the Core Platform, which is now going to take sort of the benefit of pricing and bundling across both segments.

p. 5 · Read in context →

The monetization mechanic: an in-context paywall at the moment of engagement pulls attach forward from months later — and drives that 40%.

Aman Bhutani, CEO: Over the last quarter or two, we started to put up paywalls where, along with that engagement, if, for example, a customer got a coming soon page and wanted to customize it a little bit, if they wanted to do more, a paywall would appear and say you need to buy a subscription or websites plus marketing. It's possible that a customer would have bought it anyway, two months or three months down the line, and we would have gotten that attachment. But what Airo offers is the ability for us to paywall right there, getting the customer to make that decision. That paywall is connected to the 40% that I talked about today.

p. 7 · Read in context →

Engagement, not discovery, is the quality metric — and Airo was deliberately kept out of the 3-year plan to build the funnel first.

Aman Bhutani, CEO: As we spend in marketing, discovery will definitely go up, but we don't want engagement as a percentage to drop. Engaged customers enter the monetization phase in a much more favorable manner than non-engaged customers. Metrics like attached conversion do much better for engaged users than they do for non-engaged users. That's if you will, the quality metric. […] we purposefully put Airo outside of the three-year planning because we wanted to build a very large mode of discovery and engagement. That very large mode will generate sort of recurrence for years to come.

p. 10 · Read in context →

On the WP Engine–Automattic WordPress feud: GoDaddy calls WordPress 'here to stay,' casting itself as a top contributor, not a bystander.

Clarke Jeffries (Piper Sandler); Aman Bhutani, CEO: there is a notable market event in the last quarter, a disagreement between a Managed WordPress vendor and the largest contributor to WordPress. Aman, do you see that as largely irrelevant to the long-term progress of WordPress? Have you seen any kind of conversations with your customers or partners that reacted to that? […] Our focus is really to build magical experiences on top of the WordPress platform, which is the largest content management system in the world. We believe that WordPress is here to stay. We are one of the top contributors and we're part of the WordPress community. We want to harness the power of WordPress and provide seamless experiences for our users, including enhanced functionalities.

p. 14 · Read in context →

Q4 2023 Earnings Call — February 13, 2024

The foundational call: the A&C / Core Platform model, the attach → retention → LTV engine, Airo's launch and first monetization proof, payments scaling, and the free-cash-flow-per-share North Star with its buyback engine. · Open the full transcript →

Airo's first controlled test: the test cohort out-monetized the control group at once — via attach and a shift to higher-margin products.

Aman Bhutani, CEO: I am happy to share that in a controlled experiment, customers that were part of the first test cohort for the Airo experience monetized at rates higher than those customers in the control group that were not exposed to the Airo experience. The increased monetization was due to attach and shifting the mix towards higher price and higher margin products.

This is particularly encouraging because significant customer experience changes like Airo typically take many months of iterative improvement to outperform the control group.

p. 2 · Read in context →

The commerce proof: GoDaddy can sell payments into its own base — 2023 annualized GPV grew 125%, its largest driver of payments growth.

Aman Bhutani, CEO: On Commerce, over the last year we proved that we can sell our payments solutions into our customer base, and it was the largest driver of GPV growth last year. In fact, annualized GPV for 2023 exceeded our expectations and grew a 125% year-over-year.

p. 2 · Read in context →

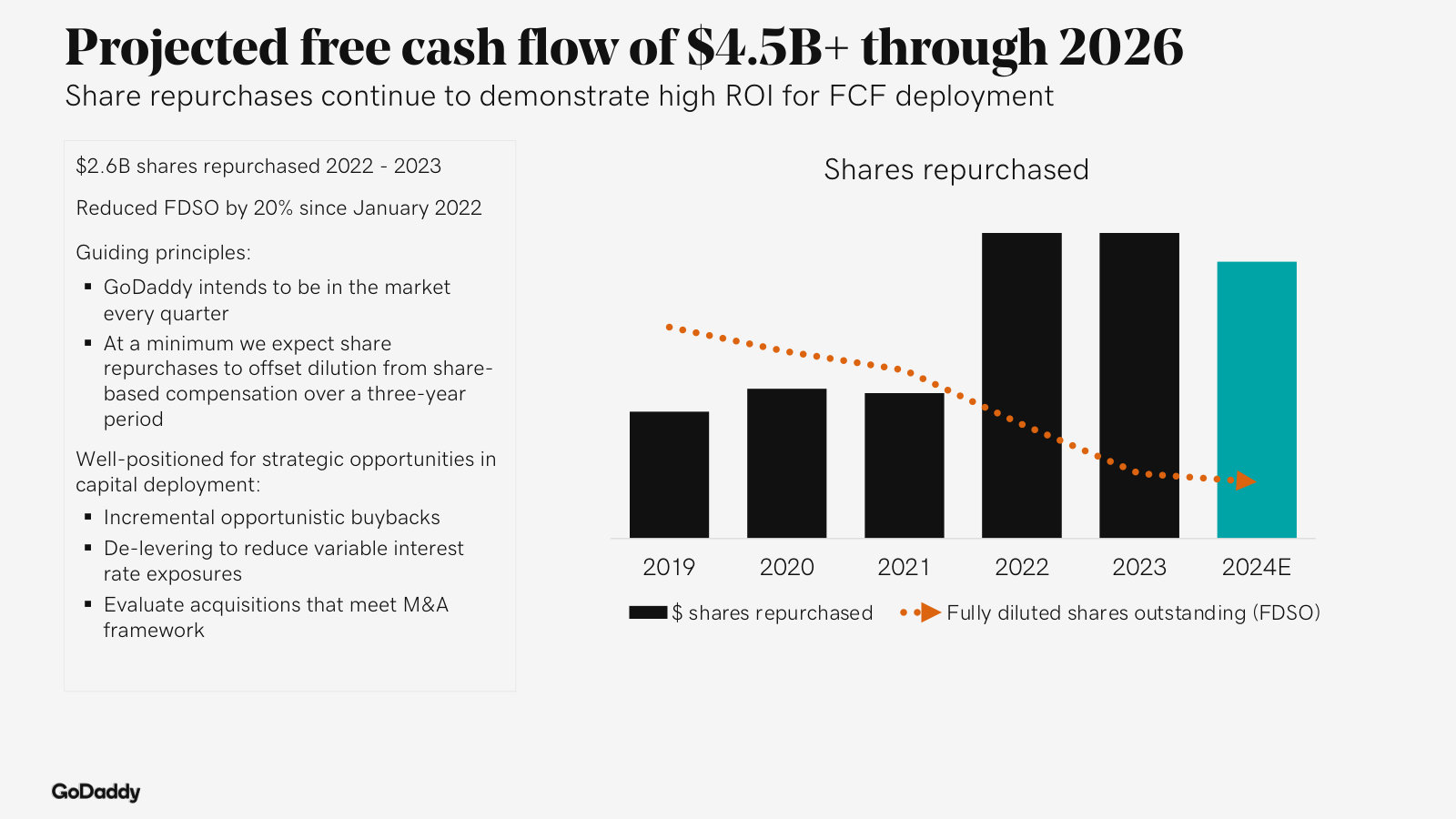

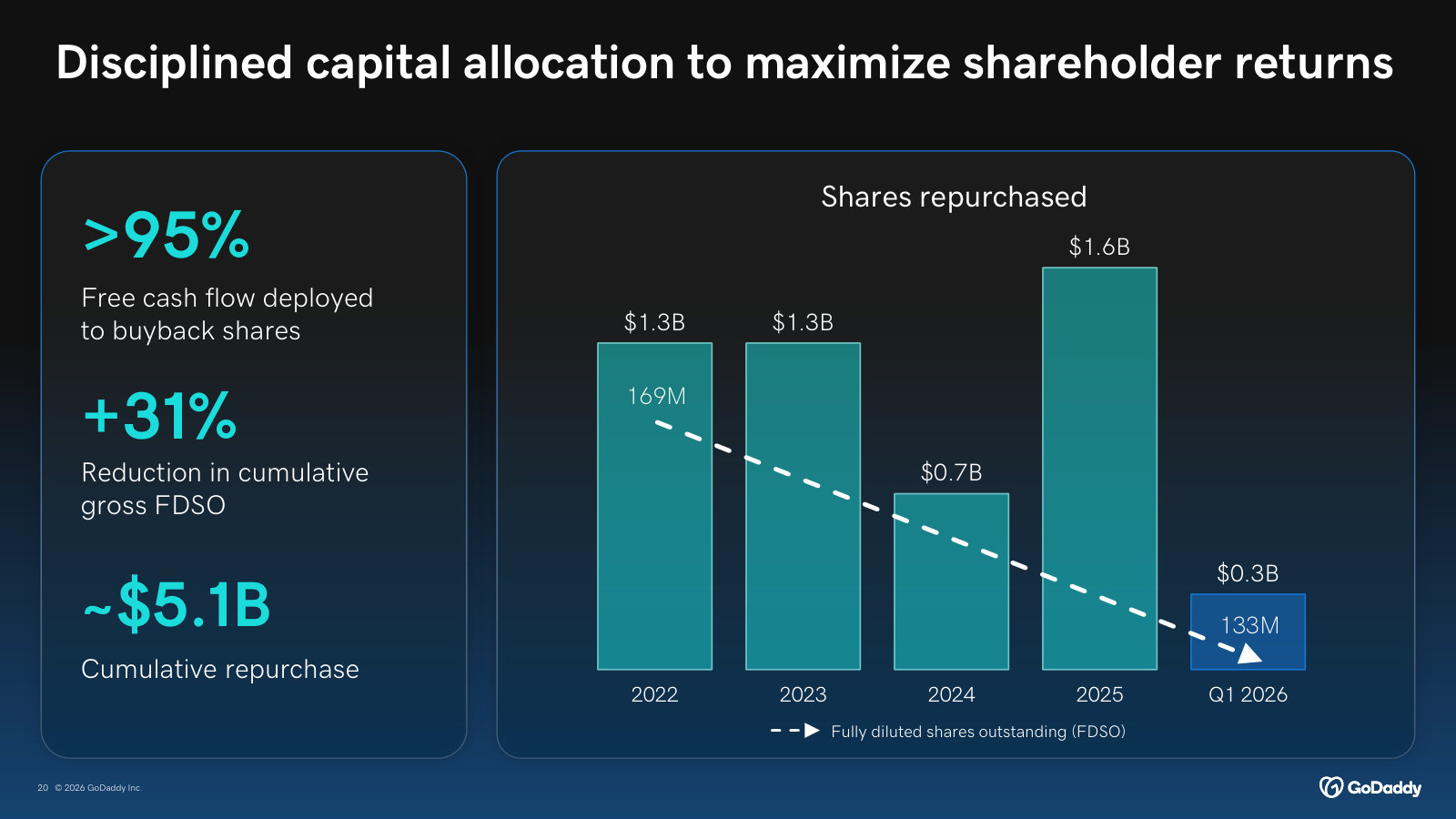

The capital-return engine: $2.6B / 34.2M shares retired cut the diluted count over 20% — the three-year target hit ahead of schedule.

Mark McCaffrey, CFO: Additionally, the cumulative shares repurchased under our current authorizations totaled $2.6 billion, representing 34.2 million shares retired. This reduced our fully diluted shares outstanding since the inception of these authorizations by over 20%, achieving our three-year targeted reduction ahead of schedule.

Our buybacks over the last two years have driven impressive ROI for this capital outlay, demonstrating our disciplined capital allocation framework and dedication to driving long-term shareholder value.

p. 3 · Read in context →

The core economic engine: second- and third-product attach powers high-margin A&C; retention rises from 85% to 'almost a customer for life.'

Mark McCaffrey, CFO: we’re seeing the demand move to that second product much faster than we had ever seen. And then now we’re seeing it to the third product much faster than we’ve ever seen. So that shows up in our A&C growth. That’s our higher profitability segment as well. […] We’ve talked about once we get to the second product, our average retention is 85%, but it goes up from there. If we get customers to a third product, it goes up significantly.

It’s almost a customer for life.

p. 7 · Read in context →

More calls

Q2 2025 Earnings Call — August 7, 2025 · 11 pages · The first hard quantification of the $500+ 'near-perfect-retention' cohort (~9% of the base) and the most direct rebuttal to AI 'vibe coding' competition; the .co registry walk-away as a discipline signal. · Open →

Q1 2025 Earnings Call — May 1, 2025 · 10 pages · The new $3B buyback authorization and sub-3x leverage target, plus the clearest walk-through of the free-Airo → Airo Plus upsell mechanic. · Open →

Q4 2024 Earnings Call — February 13, 2025 · 16 pages · Full-year 2024 results against the March-2024 Investor Day targets — the margin and free-cash-flow print that reset the bar for 2025. · Open →

Q2 2024 Earnings Call — August 1, 2024 · 13 pages · Capital-allocation priorities ranked against the FCF North Star, and the three structural EBITDA-margin tailwinds spelled out. · Open →

Q1 2024 Earnings Call — May 2, 2024 · 13 pages · The first call after the March 2024 Investor Day, testing the newly framed North Star and long-term margin targets. · Open →

Q3 2023 Earnings Call — November 2, 2023 · 12 pages · The pre-Airo integration era: margin expansion from unifying the software platform and rationalizing non-core hosting. · Open →

Q2 2023 Earnings Call — August 3, 2023 · 12 pages · Early evidence that the platform unification was lifting attach and A&C margin, ahead of the Airo launch. · Open →

Q1 2022 Earnings Call — May 5, 2022 · 29 pages · Where GoDaddy reframed reporting into two segments (Applications & Commerce and Core Platform) and laid out the three-year plan and $6+ FCF-per-share goal. · Open →

GoDaddy Inc.'s annual reports contain management's most considered account of the business. These are the sections, passages and visual pages worth opening in the originals preserved in Sources.

GoDaddy Inc. — FY2025 Annual Report (Form 10-K) — FY2025

The latest 10-K: how GoDaddy frames its business, its two segments, the drivers behind 2025 results, and the risks most specific to a domains-and-hosting model. · Open the full document →

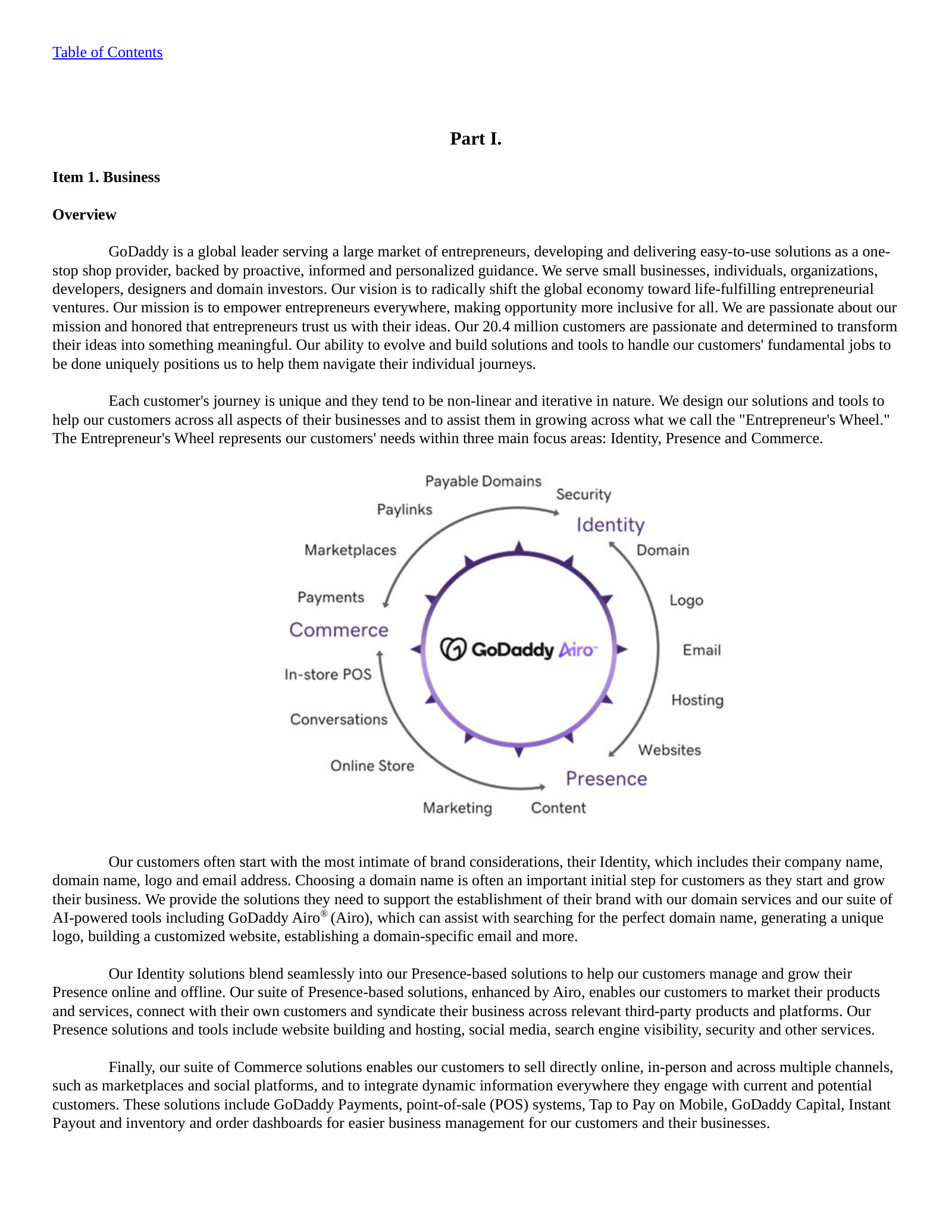

Item 1. Business — Overview — p. 7 · Read the full section →

Management's own one-paragraph statement of what GoDaddy is, who it serves, and the scale of its customer base.

The business in management's words — a one-stop shop for 20.4 million entrepreneurs.

GoDaddy is a global leader serving a large market of entrepreneurs, developing and delivering easy-to-use solutions as a onestop shop provider, backed by proactive, informed and personalized guidance. […] Our 20.4 million customers are passionate and determined to transform their ideas into something meaningful.

p. 7 · Read in context →

Item 1. Business — Our Solutions and Experiences: Applications & Commerce and Core Platform — p. 11 · Read the full section →

Defines the two reporting segments and what each sells — the Core Platform (domains, hosting) still ~62% of revenue, A&C the growth engine.

Applications & Commerce — website building, e-commerce, marketing, email and productivity.

Bringing an idea to life online, establishing and maintaining a presence and continuing to grow requires the right tools and products. Website building solutions, e-commerce tools, digital marketing capabilities, email and other productivity solutions within the A&C segment are designed to help our customers start, grow and scale their presence and their businesses.

p. 11 · Read in context →

Core Platform — domains, aftermarket, hosting and security; ~62% of total revenue.

Our Core Platform products meet customers at a common starting place, establishing an exclusive, uniquely branded identity through domain registrations and renewals and an aftermarket domain platform. We also provide adjacent offerings to assist customers in building and maintaining a presence online, including website hosting and website security. During the years ended December 31, 2025, 2024 and 2023, we derived approximately 62%, 64% and 66% of our total revenue, respectively, from sales of our Core Platform products.

p. 15 · Read in context →

Item 1A. Risk Factors — Evolving technologies (AI) and changes in customer behavior may impact demand for and value of our products — p. 48 · Read the full section →

The most existential risk for a domains-and-websites business: AI and alternative systems could erode the need to register a domain at all.

As AI and social channels rise, domains and websites "may become less prominent, and their value may decline."

As reliance on social media channels, applications and AI-powered tools increases, domain names, websites and online stores and marketplaces may become less prominent, and their value may decline. […] The widespread acceptance of any alternative system, such as mobile applications, AI-powered products and tools or closed networks, could eliminate the need to register a domain name or to establish an online presence and could materially and adversely affect our business.

p. 50 · Read in context →

Item 1A. Risk Factors — We face significant competition, which we expect will continue to intensify — p. 50 · Read the full section →

GoDaddy competes across every layer of its portfolio — registrars, hosts, website builders, payments — and now against AI-native entrants.

A broad portfolio means competition on every front, from point solutions to full-stack rivals.

The market for our products and services is highly competitive, and we expect this competition to continue in the future as existing and new competitors introduce new solutions or enhance existing solutions. […] Our competitors include providers of domain registration services, web-hosting solutions, website creation and management solutions, e-commerce enablement providers, payment facilitation providers, cloud computing service and online security providers, alternative web presence and marketing solutions providers and providers of productivity tools such as business-class email.

p. 50 · Read in context →

Item 1A. Risk Factors — A delay in access to new TLDs (ICANN) could adversely impact our business — p. 79 · Read the full section →

The registrar model depends on ICANN policy; the 2026 "Next Round" of new gTLDs is a structural dependency unique to this industry.

Domain access hinges on ICANN — participation in the upcoming Next Round is a competitive necessity.

ICANN has periodically authorized the introduction of new TLDs and made domain names related to them available for registration. […] Our competitive position depends in part on our ability to gain access to and meaningfully participate in new TLDs opportunities, including the Next Round.

p. 79 · Read in context →

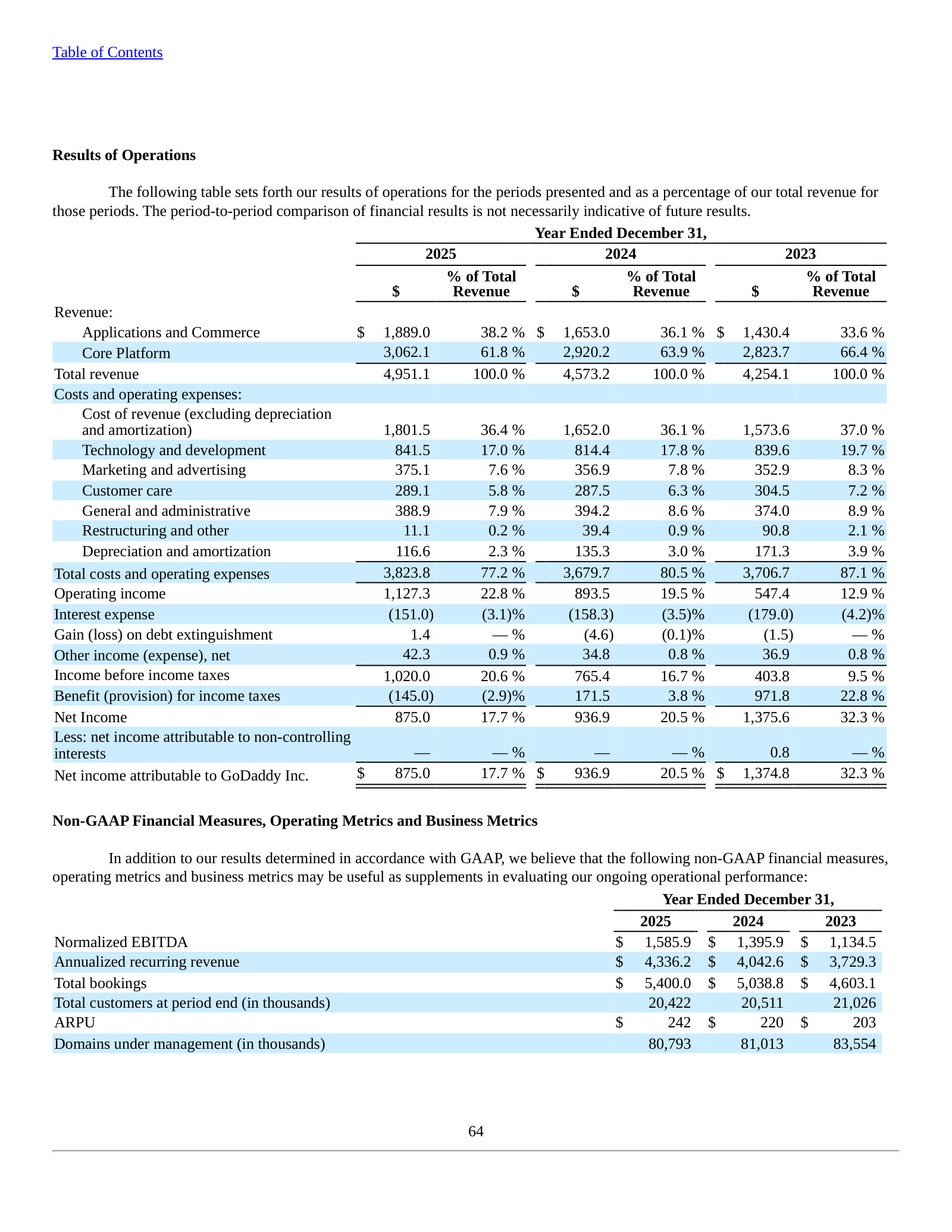

Item 7. Management's Discussion and Analysis — Results of Operations — p. 113 · Read the full section →

Where management explains what actually drove 2025: revenue to $4.95bn and operating margin to 22.8%, plus the initiatives behind it.

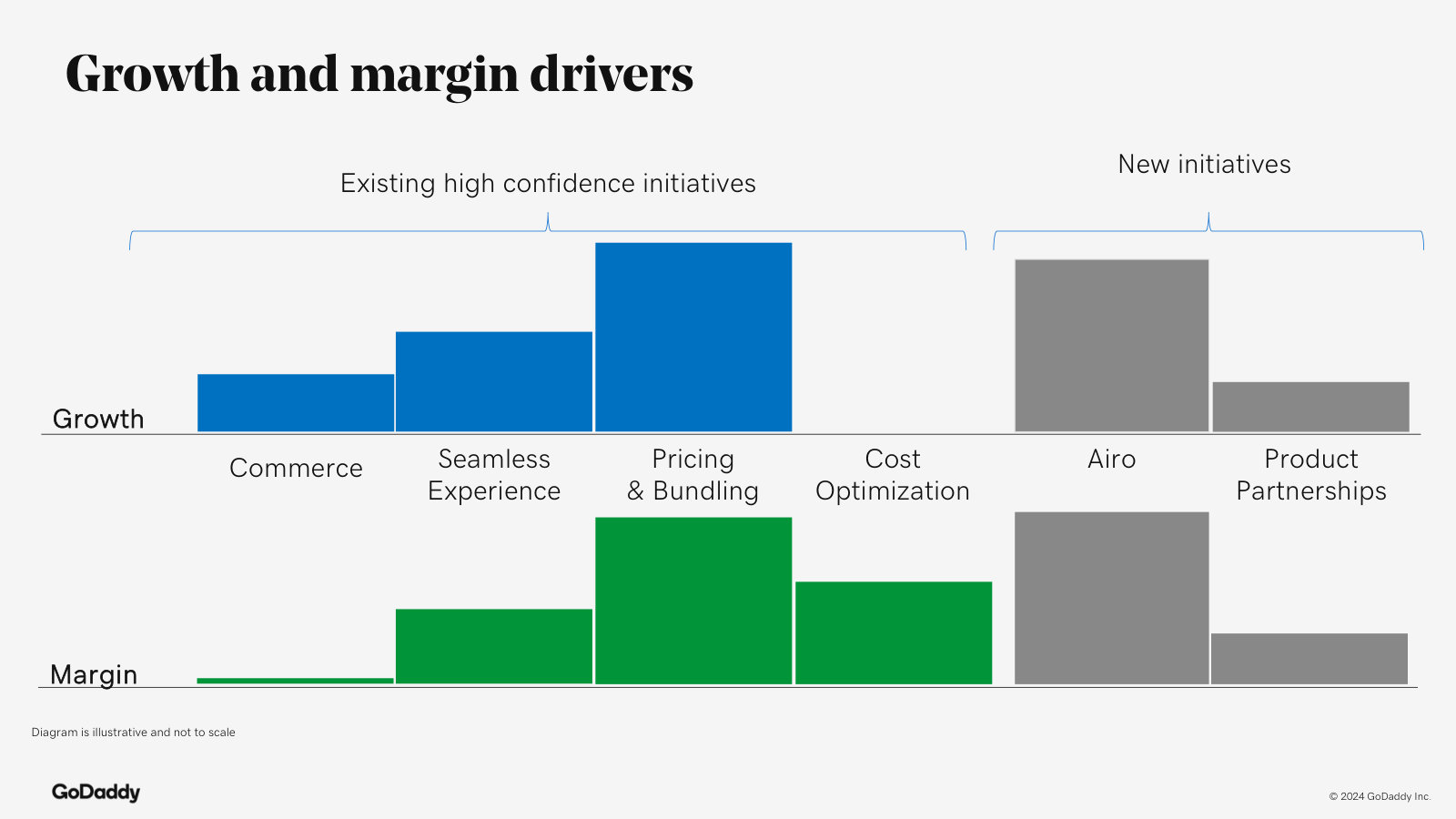

The four levers management credits for growth: seamless tech/Airo, cost optimization, pricing & bundling, commerce.

The primary factors driving growth in our business are our seamless technology experience, cost optimization and retention of high intent customers, pricing and bundling, and commerce.

p. 114 · Read in context →

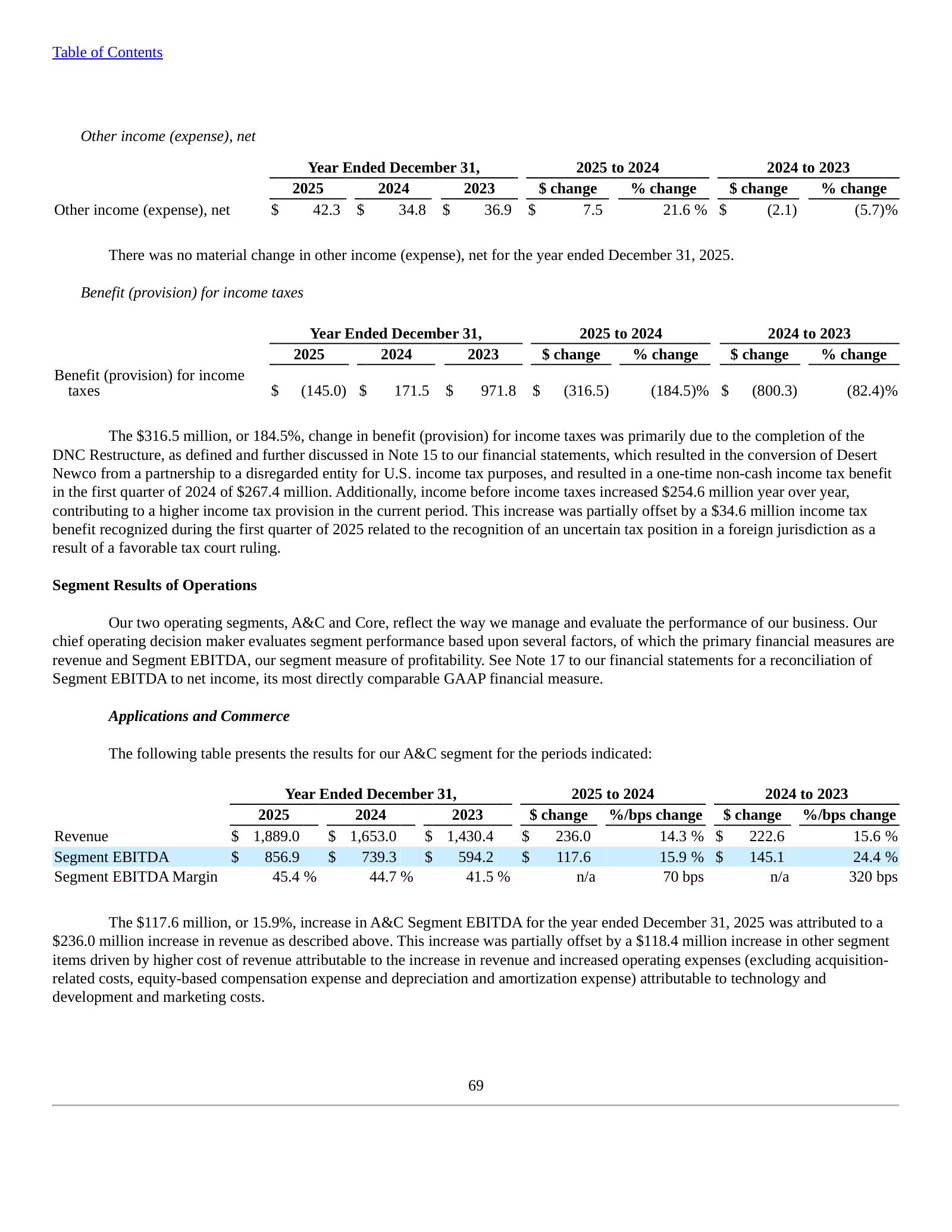

Item 7. Management's Discussion and Analysis — Segment Results of Operations — p. 125 · Read the full section →

Segment EBITDA reveals where profit is made: A&C carries a ~45% margin versus Core's ~33% — the mix story behind the P&L.

How management measures the two segments — revenue and Segment EBITDA.

Our two operating segments, A&C and Core, reflect the way we manage and evaluate the performance of our business. Our chief operating decision maker evaluates segment performance based upon several factors, of which the primary financial measures are revenue and Segment EBITDA, our segment measure of profitability.

p. 125 · Read in context →

Item 7. Critical Accounting Policies and Estimates — Revenue Recognition — p. 130 · Read the full section →

The policy that defines the subscription model — domain and renewal revenue recognized ratably, feeding deferred revenue and bookings.

GoDaddy Inc. — FY2021 Annual Report (Form 10-K) — FY2021

Included to show a real structural evolution: in FY2021 GoDaddy reported as a single segment; by FY2022 it split into Applications & Commerce and Core Platform. · Open the full document →

Item 1. Business — Overview — p. 7 · Read the full section →

The earlier self-description — 21.2 million customers and a different framing before the Airo/agentic-AI and commerce emphasis of today.

GoDaddy in 2021 — "everyday entrepreneurs" and 21.2 million customers.

GoDaddy is a global leader in serving a large market of everyday entrepreneurs, delivering simple, easy-to-use products, and outcome-driven, personalized guidance to small businesses, individuals, organizations, developers, designers and domain investors. […] Our 21.2 million customers are passionate, everyday entrepreneurs with vibrant ideas, who are determined to make their way in the world and to transform their ideas into something meaningful.

p. 7 · Read in context →

Notes to Consolidated Financial Statements — Segment — p. 137 · Read the full section →

The "before" of the segment redefinition: in 2021 the CEO reviewed the company on a consolidated basis — a single reportable segment.

One segment in 2021 — the structure later split into A&C and Core.

As of December 31, 2021, our chief operating decision maker was our Chief Executive Officer who reviews financial information presented on a consolidated basis for purposes of allocating resources and evaluating financial performance for the entire company. Accordingly, we have a single operating and reportable segment.

p. 137 · Read in context →

More annual reports

GoDaddy Inc. — FY2024 Annual Report (Form 10-K) — FY2024 · 197 pages · Prior-year 10-K with the same two-segment structure — useful for year-over-year comparison of segment revenue and margins. · Open →

GoDaddy Inc. — FY2023 Annual Report (Form 10-K) — FY2023 · 224 pages · The year restructuring charges and cost actions began driving margin expansion; useful baseline for the profitability turn. · Open →

GoDaddy Inc. — FY2022 Annual Report (Form 10-K) — FY2022 · 211 pages · The first 10-K under the two-segment (Applications & Commerce / Core Platform) structure that GoDaddy still uses today. · Open →

Competitors describe GoDaddy Inc.'s market in their own filings and calls. These verified passages and visual pages show where their strategies meet, using source documents preserved in Sources.

Wix.com (WIX)

The most direct competitor to GoDaddy's website-builder and web-presence business — a SaaS platform selling website creation, domains and commerce tools to the same small businesses and entrepreneurs. It is the one peer that names GoDaddy in its filings.

Wix's 20-F competition section names GoDaddy by name — as a large domain-registration and hosting company that also lets a business owner build a website — and flags generative-AI website builders as an emerging overlap.

several large service companies that primarily offer domain registration and hosting services, such as GoDaddy, provide the ability for a business owner to build a website using their tools or have one built by their workforce. Moreover, newly emerging technologies that utilize AI may also offer services that overlap with certain solutions we offer, including the emergence of generative AI website builders.

p. 106 · Read in context →

Wix's characterization of the shared market for website design-and-management software as 'highly fragmented,' with no incumbent offering a fully integrated solution — the space GoDaddy's Websites + Marketing also targets.

The market for providing web-based website design and management software is evolving and highly fragmented today. We believe no provider currently offers a comprehensive, customizable, fully integrated workflow solution to create and manage a professional digital presence comparable to ours.

p. 106 · Read in context →

IONOS Group (IOS)

A European web-hosting, domains and cloud provider for SMEs whose 'Web Presence & Productivity' line — domain registration, hosting, AI website builders, email and commerce — maps almost one-for-one onto GoDaddy's core offering, and which competes with GoDaddy in North America as well as Europe.

IONOS's Web Presence & Productivity portfolio — domain registration, web hosting, AI-powered website builders, e-commerce, email, marketing and SEO — maps closely onto GoDaddy's own product stack for small businesses.

In the Web Presence & Productivity division, IONOS offers professional solutions for online presence, such as domain registration, web hosting, website builders powered by artificial intelligence, and dedicated servers. This is complemented by additional productivity tools (e.g., e-commerce, email, and marketing applications) as well as supplementary services such as search engine optimization, business applications, and storage and security solutions.

p. 5 · Read in context →

IONOS's stated scale and positioning — a base of over six million customers and a claim to be a leading SME digitalization partner — a reference point against GoDaddy's own customer and share narrative.

As one of the leading providers and preferred digitalization partners for small and medium-sized enterprises (SMEs), IONOS is exceptionally well-positioned to benefit sustainably from this structural market growth. […] A central pillar and a decisive competitive advantage is its loyal customer base of over six million customers worldwide.

p. 53 · Read in context →

IONOS positions itself as a 'one-stop shop' for SMEs, citing strong positions in Germany, Spain, the UK and Austria — the European strongholds it defends against GoDaddy's US base.

IONOS clearly positions itself as a “one-stop shop” for digital transformation. The company operates in a structurally growing market driven by megatrends such as cloud migration and, increasingly, by agentic A (AI agents). […] With strong market positions in key markets such as Germany, Spain, the United Kingdom, and Austria, the Group is exceptionally well-positioned.

p. 8 · Read in context →

Tucows (TCX)

A top global domain registrar and GoDaddy's clearest rival in the domains business — its OpenSRS, Enom and Ascio wholesale registrars and Hover retail brand compete directly for domain registrations. Its Ting fiber and Wavelo telecom units do not overlap with GoDaddy and are excluded here.

Tucows' claim to a strong position in the wholesale domain-registration and email markets behind its OpenSRS, Ascio and Enom brands — the reseller-friendly channel where it competes with GoDaddy rather than in retail website-building.

We believe that we are well positioned in the wholesale domain registration and email markets due in part to our highly-recognized “Tucows”, “OpenSRS”, “Ascio” and “Enom” brands and the respect they confer on us as a defender of end-user rights and reseller-friendly approaches to doing business. We were among the first group of 34 registrars to be accredited by ICANN in 1999

p. 8 · Read in context →

Tucows quantifies its wholesale distribution moat: a network of more than 34,000 resellers across 200 countries selling white-label domains — a channel-led model distinct from GoDaddy's retail-direct approach.

Tucows Domains generates revenues primarily from the registration fees charged to resellers in connection with new, renewed and transferred domain name registrations. […] Our primary distribution channel is a global network of more than 34,000 resellers that operate in 200 countries […] providing the broadest portfolio of gTLD and the country code top-level domain options and related services, a white-label platform that facilitates the provisioning and management of domain names

p. 7 · Read in context →

Tucows' domain brand stack — OpenSRS, Enom, Ascio, EPAG and Hover, spanning wholesale and retail registration — the direct product collision with GoDaddy's registrar business.

Tucows Domains includes wholesale and retail domain name registration services, as well as value-added services derived through our OpenSRS, Enom, Ascio, EPAG and Hover brands.

p. 6 · Read in context →

GMO Internet Group (9449)

Japan's leading domain registrar and web-hosting group — the GoDaddy-analog in its home market, selling domain registration (Onamae.com), hosting and servers to the same small-business customers. Its footprint is concentrated in Japan and its payment, security and crypto arms fall outside GoDaddy's business.

GMO frames its domains-hosting-servers stack — the same registrar-plus-hosting bundle GoDaddy sells — as the number-one service in each layer of the Japanese market.

GMO Internet Group management, Q2 FY2025 results presentation: We have developed a wide range of services from infrastructure areas such as Internet access, domain names, cloud computing, and rental servers to value-added areas such as payment settlement and online store support. Each is the number one service, and by generating synergies with each other, we have achieved sustainable growth.

p. 17 · Read in context →

GMO reframes the registrar/hosting battleground around AI-agent traffic, positioning MCP and API support as a new competitive front GoDaddy must also contest.

GMO Internet Group management, Q1 FY2026 results presentation: The main users of the Internet are rapidly shifting from humans to Al […] what is required of our group is to become a company that AI will choose. To this end, we are working on MCP support and API support.

p. 12 · Read in context →

Shopify (SHOP)

The leading commerce platform for entrepreneurs and small businesses — adjacent to GoDaddy's domains/web-presence core but a direct competitor to GoDaddy's growing Applications & Commerce segment (online-store creation, payments) and to its 'help entrepreneurs start a business' positioning.

Shopify's self-description as commerce infrastructure that makes it easier to 'start, run and grow a business' for merchants from aspirational entrepreneurs upward — the same start-a-business pitch GoDaddy makes to its small-business base.

Shopify provides essential internet infrastructure for commerce. Shopify's all-in-one platform makes it easier to start, run and grow a business, powering sales online, in store, and everywhere in between. […] We believe we can help merchants of all verticals and sizes, from aspirational entrepreneurs to companies with large-scale, direct-to-consumer or business to business ("B2B") operations, or both, realize their potential at all stages of their business life cycle.

p. 7 · Read in context →

Shopify's merchant-solutions stack — integrated payments, working capital and shipping layered on subscriptions, monetized through Shopify Payments — mirrors the payments-and-commerce attach strategy GoDaddy is pursuing.

We offer a variety of merchant solutions to augment those provided through our subscriptions and to address the broad array of functionality merchants commonly require, including accepting payments, securing working capital and shipping. […] We principally generate merchant solutions revenues from payment processing fees and currency conversion fees from Shopify Payments, our fully integrated payment solution.

p. 9 · Read in context →

Shopify facilitated $378.4 billion of merchant GMV in 2025 (up 29% year over year) and ties its merchant-solutions revenue to that volume — the commerce flow GoDaddy's Applications & Commerce segment aims to capture a slice of.

Our merchant solutions revenues are also directionally correlated with the level of GMV facilitated through our platform.

p. 48 · Read in context →

BigCommerce (BIGC)

An open-SaaS e-commerce platform that overlaps GoDaddy's online-store and commerce offering, but which is increasingly enterprise/mid-market focused and is de-emphasizing the small-business segment where GoDaddy concentrates — useful as evidence of the limited, not head-on, overlap.

BigCommerce's account mix — 5,825 enterprise accounts alongside 'tens of thousands' of small-business accounts (on ~$351m ARR growing 3%) — shows an enterprise-weighted platform whose SMB tail is small relative to GoDaddy's mass-SMB base.

Daniel Lentz, Chief Financial Officer: BigCommerce serves 5,825 enterprise accounts, alongside tens of thousands of small business accounts.

p. 3 · Read in context →

BigCommerce states its priority is moving up-market to enterprise while its small-business base stays roughly flat — signaling it is de-emphasizing, not aggressively contesting, GoDaddy's core small-business commerce turf.

Daniel Lentz, Chief Financial Officer: The priority for us remains moving up market and focusing on enterprise accounts. […] We have tens of thousands of small business customers and we really want to find ways to expand that further.

p. 6 · Read in context →

More peer documents

WIX_annual_report_FY2023 — 324 pages · Prior-year 20-F carries the same competition section naming GoDaddy among large domain/hosting companies moving into website-building — evidence the framing is persistent, not new. · Open →

Q1_FY2026 — 26 pages · Wix management's latest call on AI-era web creation and taking share of the SMB web-presence market; the index page is partly garbled by a cookie-consent overlay, so it is shelved rather than quoted. · Open →

IOS_annual_report_FY2024 — 173 pages · IONOS's prior-year report with the same Web Presence & Productivity segment detail and customer-contract metrics for a two-year read on scale and ARPU. · Open →

9449_annual_report_FY2025 — 244 pages · GMO's annual report with the Internet Infrastructure segment's Japanese domain/hosting brands (Onamae.com, ConoHa, LOLIPOP!) and share data — mostly Japanese text and image slides, so unquotable but useful for context. · Open →

SHOP_annual_report_FY2024 — 198 pages · Shopify's prior-year 10-K for a two-year GMV and merchant-solutions trend against which to size GoDaddy's smaller commerce segment. · Open →

Q4_FY2025 — 34 pages · Shopify management's full-year call detailing merchant growth, payments penetration and the entrepreneur/SMB opportunity that frames the commerce overlap. · Open →

What GoDaddy Is, and Why the Question Is Interesting Now

GoDaddy sells the plumbing of a small business's online presence — domain names, websites, email, and payments — to 20.4 million paying customers, and it does so profitably enough to convert nearly a third of revenue into free cash. In the year to December 31, 2025 it earned $4.95 billion of revenue and $1.58 billion of free cash flow, and returned all of that cash to shareholders through buybacks. It is also a stock that fell roughly 59% from a January 2025 peak of $214 to about $89, back to where it traded in early 2024. This chapter establishes what the business is, how it earns money, and the single question the rest of this report is built to answer.

Revenue (FY2025)

Free Cash Flow (FY2025)

Normalized EBITDA Margin

Net Leverage (TTM)

Sources: FY2025 Annual Report (Form 10-K), Results of Operations and Cash Flows [1]; Q4 FY2025 earnings call [2].

The business: domains first, then everything attached to them

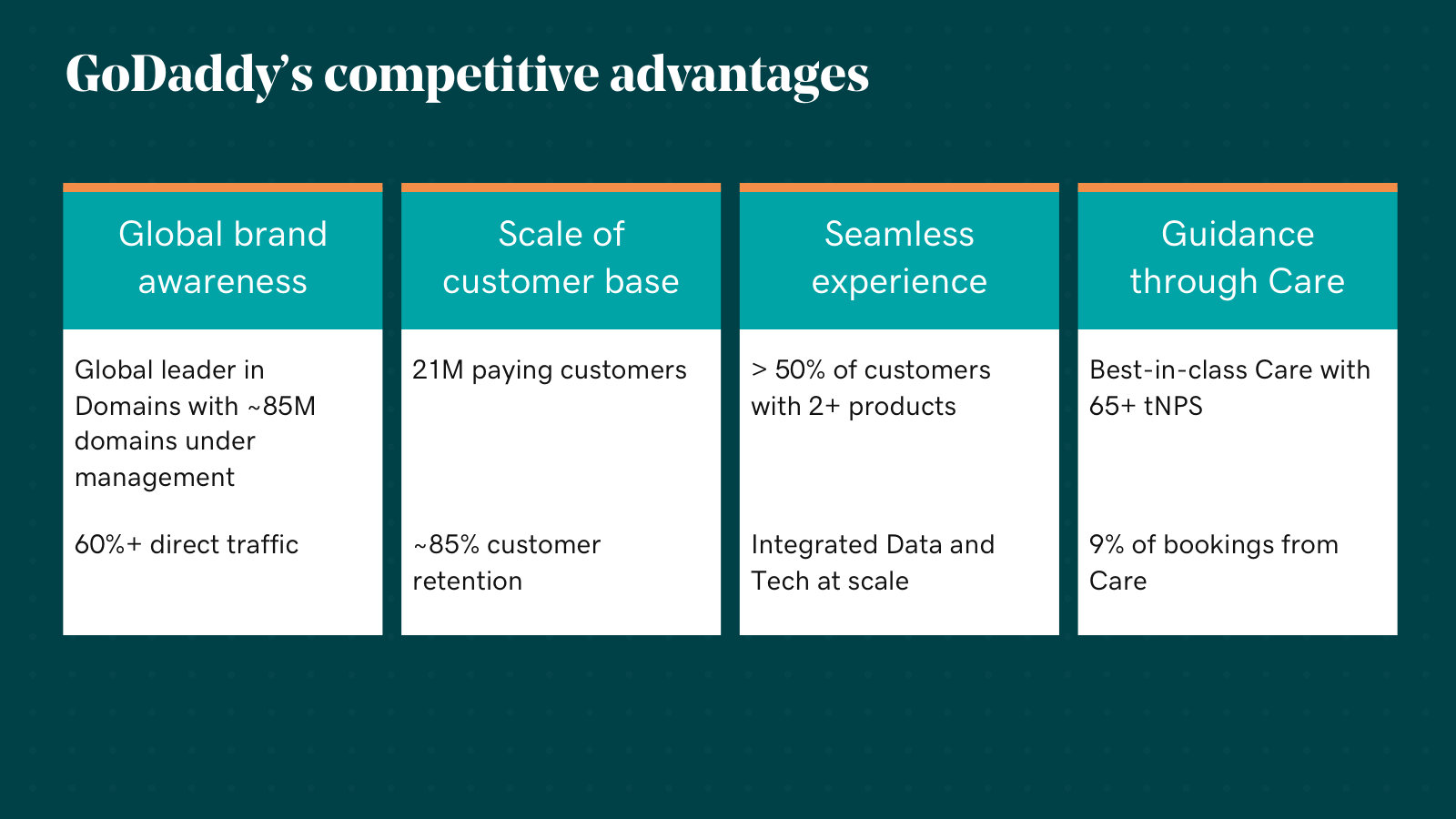

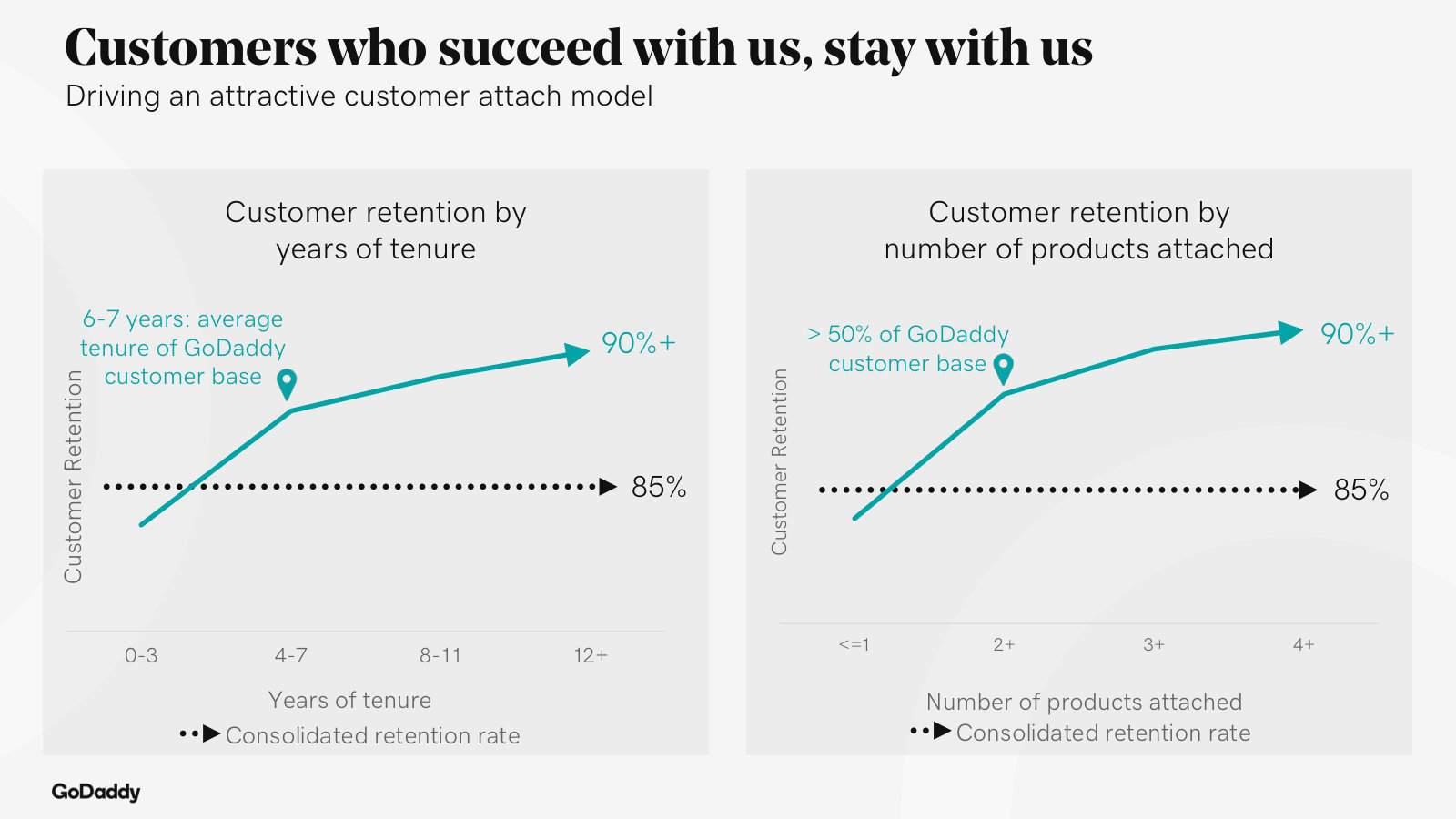

GoDaddy is the world's largest domain registrar, with roughly 81 million domains under management at the end of 2025 — about 21% of the 387 million domains registered worldwide — and a customer base of which around 94% has bought a domain from the company [3][4]. The domain is the wedge. Around it GoDaddy sells websites and website builders, hosting and security, professional email and productivity tools (largely resold Microsoft 365), and, increasingly, commerce and payments. Retention runs above 85%, and just under half the customer base — roughly a third of revenue — sits outside the United States [5].

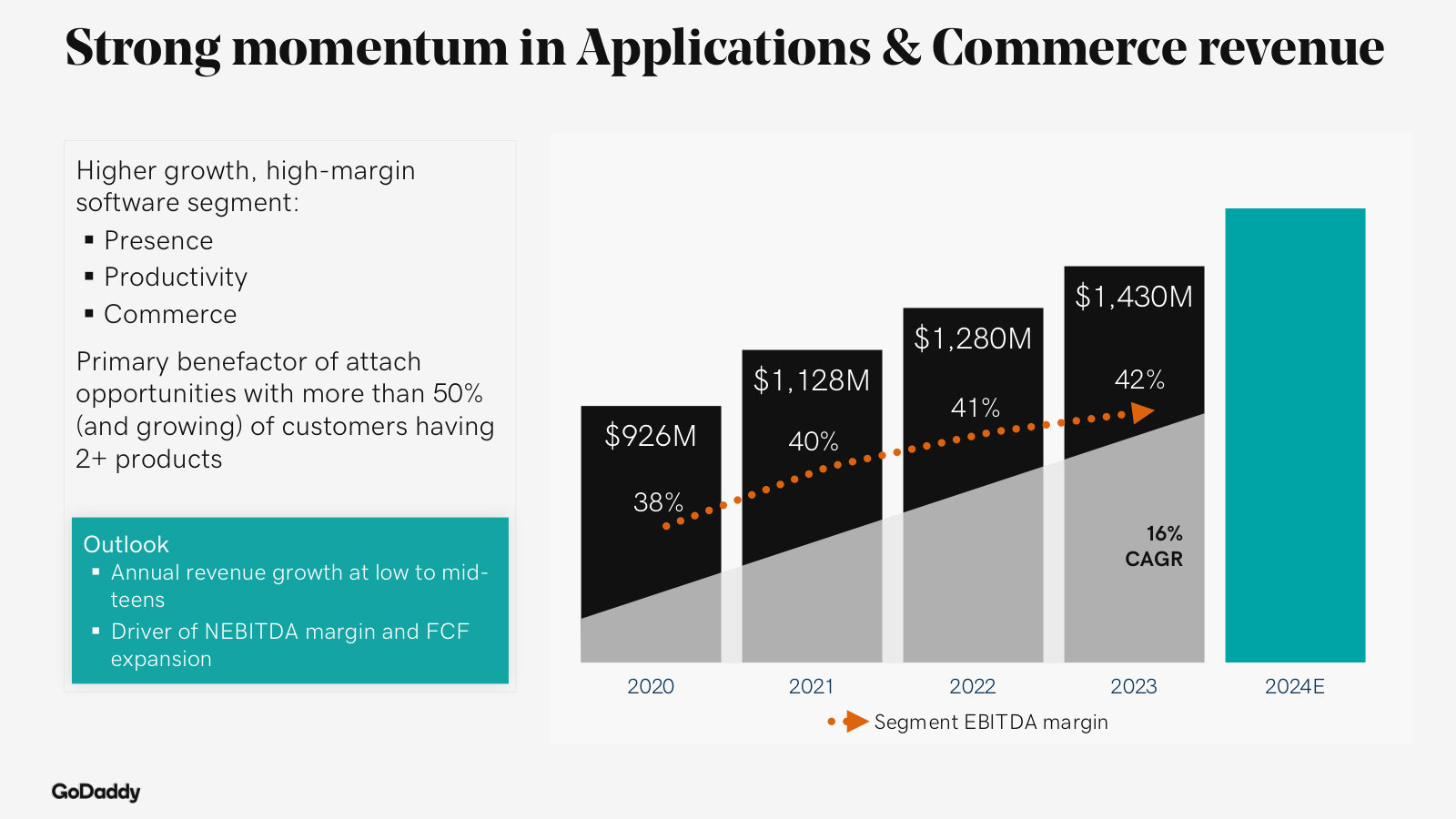

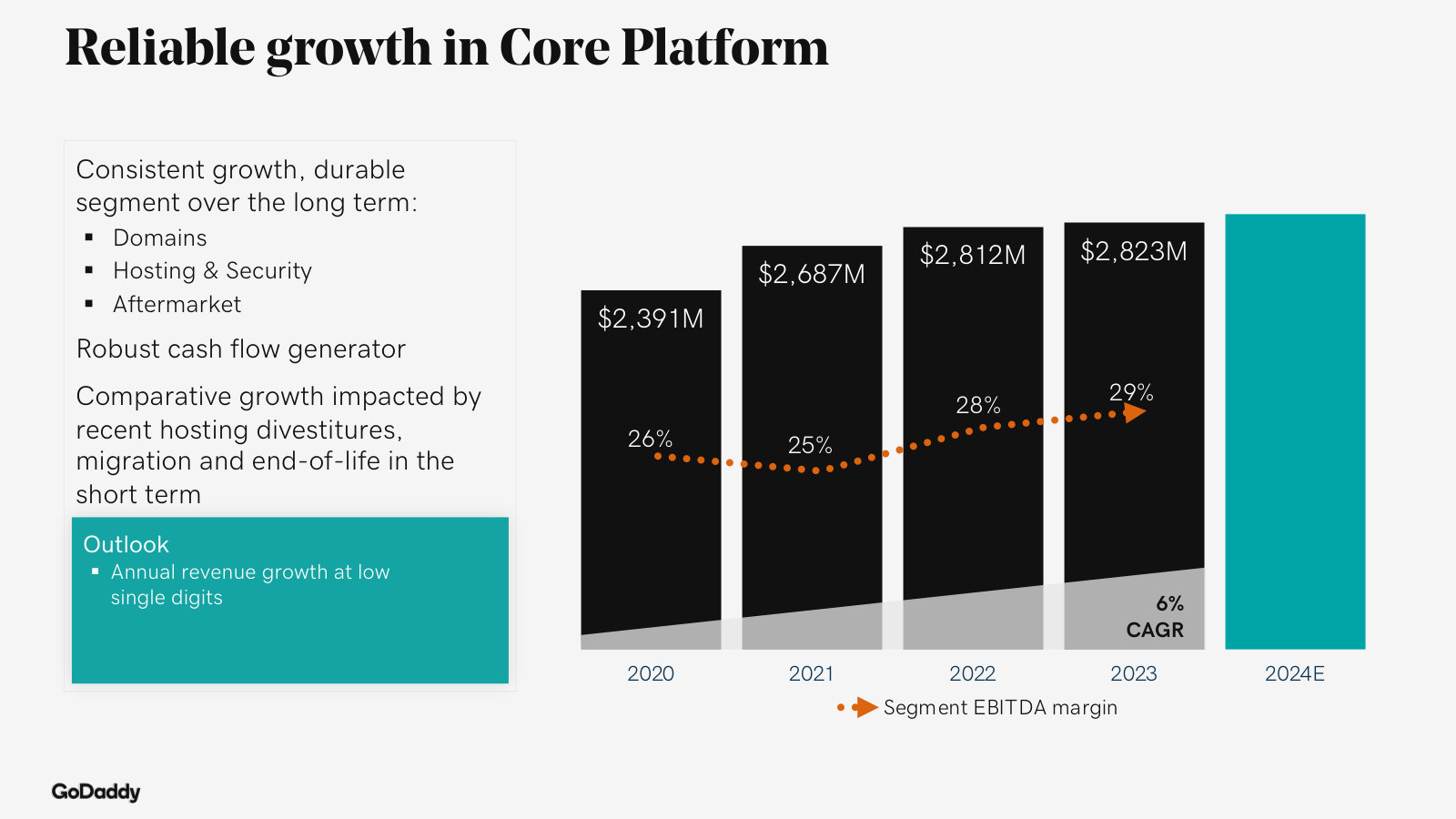

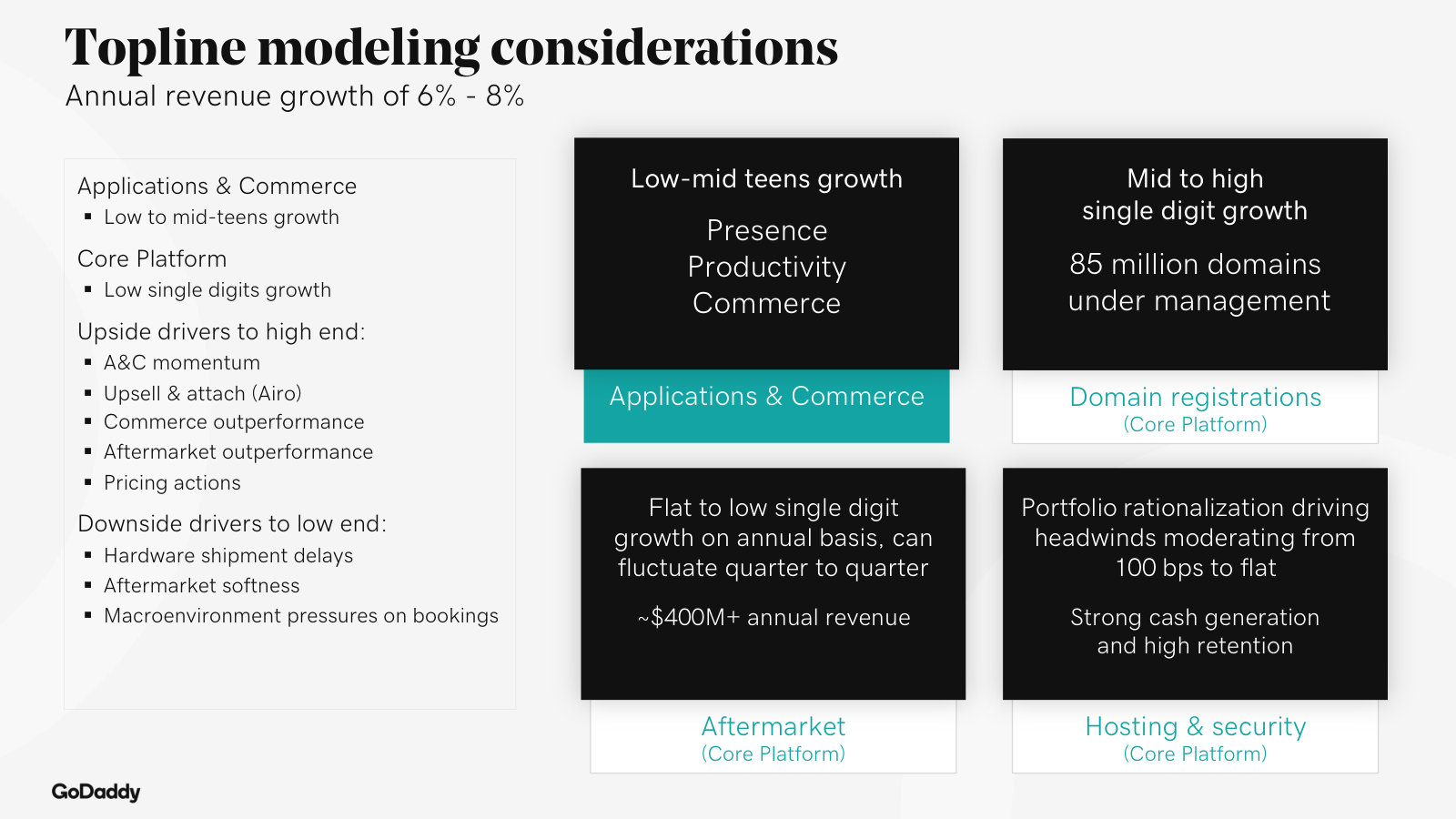

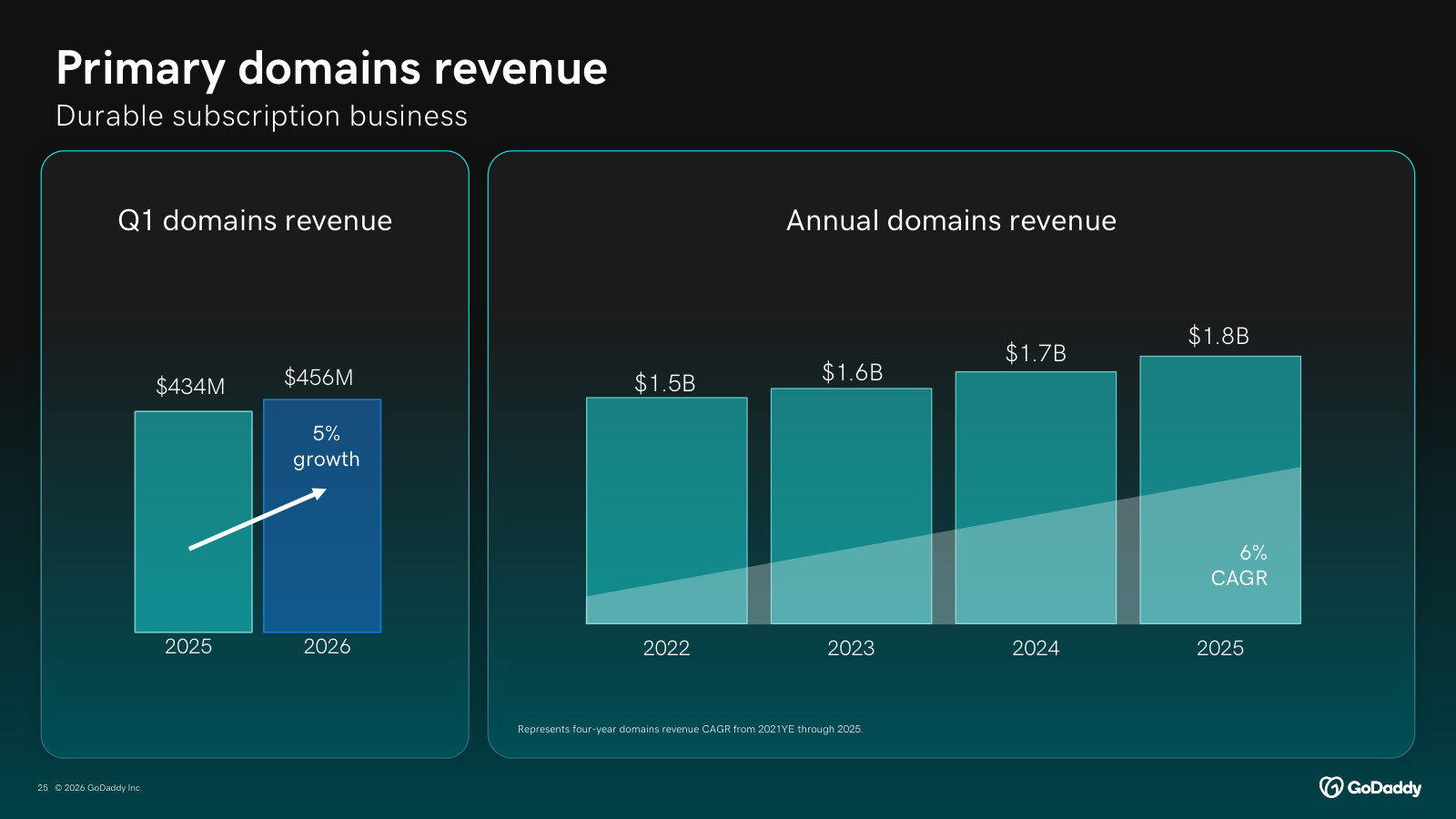

The company reports in two segments. Core Platform ($3.06 billion, 62% of revenue) is the mature engine: domains, plus a shrinking tail of legacy hosting and security. Applications and Commerce ($1.89 billion, 38%) is the growth engine: the higher-value website, email, and commerce subscriptions that carry a ~45% segment margin [6]. In FY2025, Applications and Commerce revenue grew 14.3% and Core grew 4.9%, for total growth of 8.3% [7].

Source: FY2025 Annual Report (Form 10-K), Year-Over-Year Revenue [8]; prior-year 10-Ks for FY2020–FY2023 segment history.

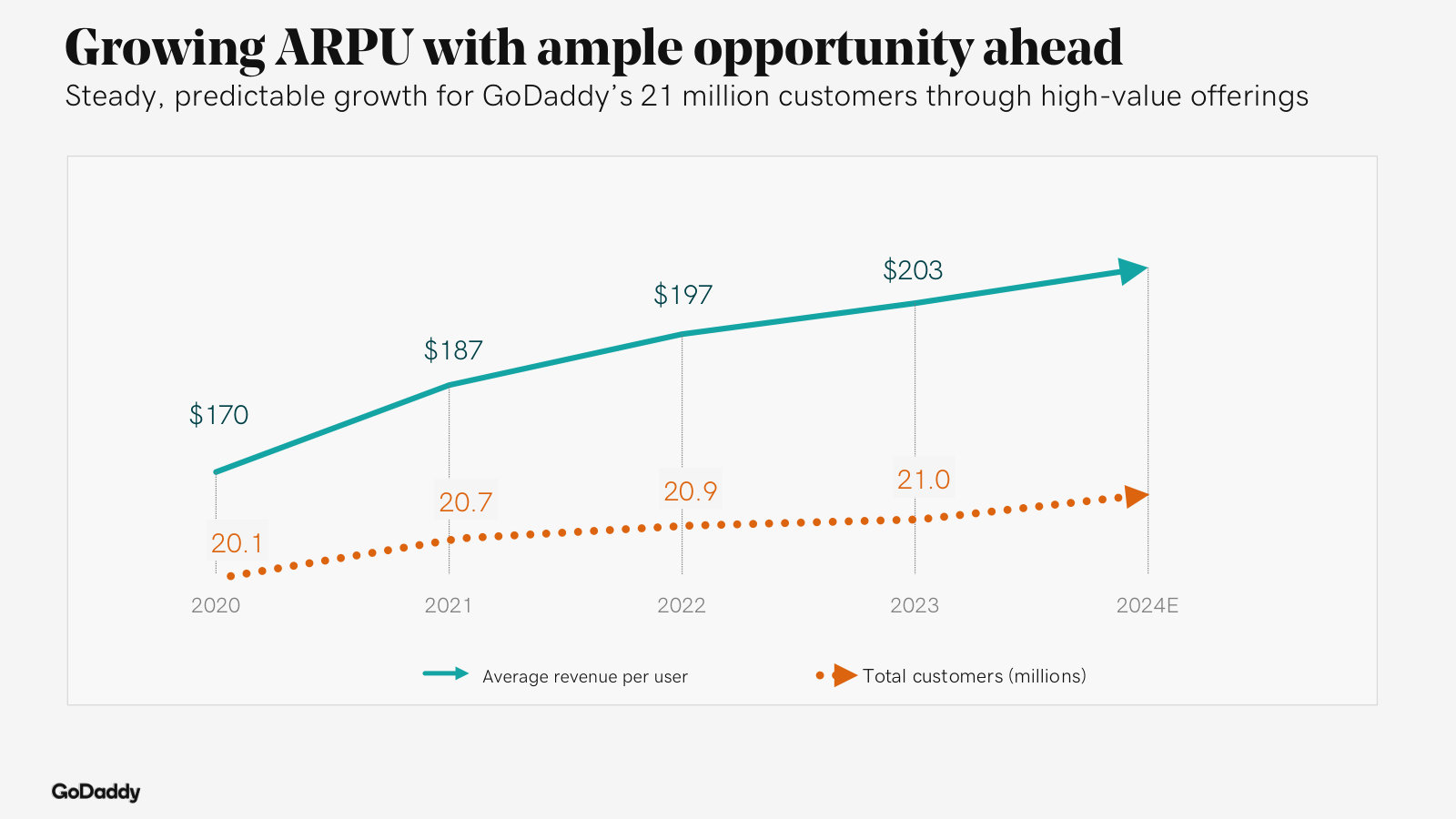

The business is overwhelmingly recurring and paid in advance. Annualized recurring revenue was $4.34 billion — about 88% of total revenue — and total bookings reached $5.4 billion, ahead of revenue because customers pay at contract inception and GoDaddy recognizes the revenue over the term [9]. That prepayment leaves $3.3 billion of deferred revenue on the balance sheet — a genuine source of float, and a reason the model throws off more cash than its accounting profit alone would suggest [10].

Growth is now monetization, not more customers

The most important thing to understand about GoDaddy's recent growth is where it comes from. It is not coming from adding customers or domains. Total customers have been flat-to-lower — 21.0 million at the end of 2023, 20.4 million at the end of 2025 — and domains under management have edged down from 83.6 million to 80.8 million over the same span. What has risen is revenue per customer (ARPU), from $203 to $242 [11].

Source: FY2025 Annual Report (Form 10-K), Operating Metrics, with prior 10-Ks for FY2020–FY2023; indexed to 2020 = 100 [12].

This is the fault line the whole investment case runs along. Read one way, it is pricing power: a sticky base that renews above 85% and pays more each year as GoDaddy attaches higher-value products — website builders, commerce, and now AI tools branded Airo. Read the other way, it is maturation: a flat-to-shrinking base of customers and domains, with growth increasingly dependent on charging the same people more, a lever with a ceiling. Both readings fit the same numbers. Which one is right is what a buyer at today's price is being asked to judge.

The cash engine and what management does with it

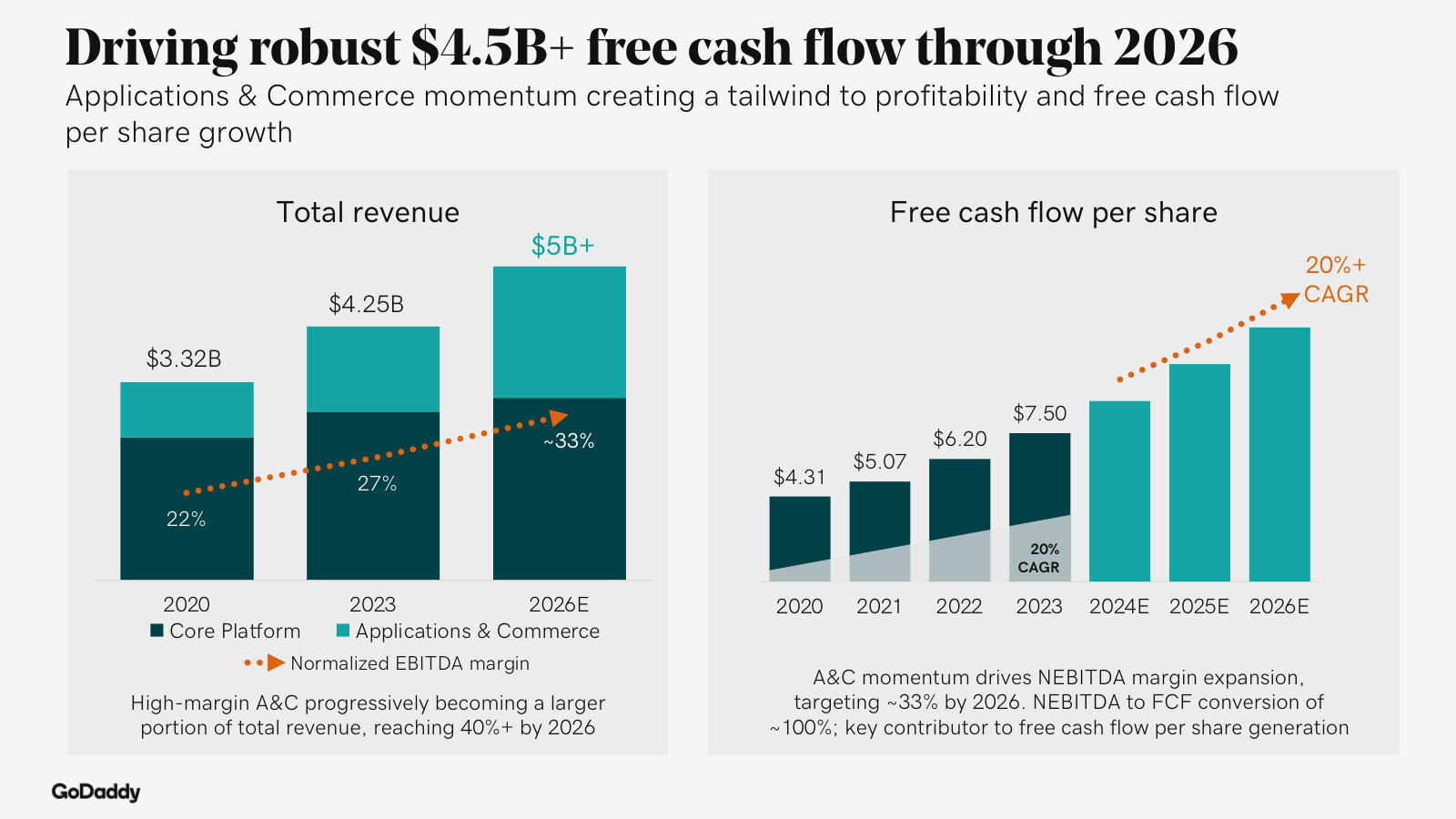

GoDaddy is asset-light to an unusual degree. Capital expenditure was $23.9 million in FY2025 — under half a percent of revenue — so operating cash flow of $1.60 billion dropped almost entirely to free cash flow of $1.58 billion, up 19% on the year [13]. Operating margin has climbed steadily, from 12.9% in FY2023 to 22.8% in FY2025 [14], and normalized EBITDA margin reached 32%, roughly 1,000 basis points higher than five years earlier [15].

Management returns essentially all of that cash through buybacks and pays no dividend. In FY2025 it repurchased 10.2 million shares for $1.6 billion — 100% of free cash flow — and over the past four years has directed more than 95% of free cash flow to repurchases [16]. The effect on the share count is real, not cosmetic: fully diluted shares have fallen roughly 33% since 2021, to 136 million at the end of 2025 and 133 million by the first quarter of 2026 [17]. That reduction more than offsets the roughly $318 million of annual equity-based compensation, which is a genuine cost the reader should net against free cash flow when judging the yield [18].

Source: FY2025 Annual Report (Form 10-K) and prior-year 10-Ks, Consolidated Statements of Cash Flows [19].

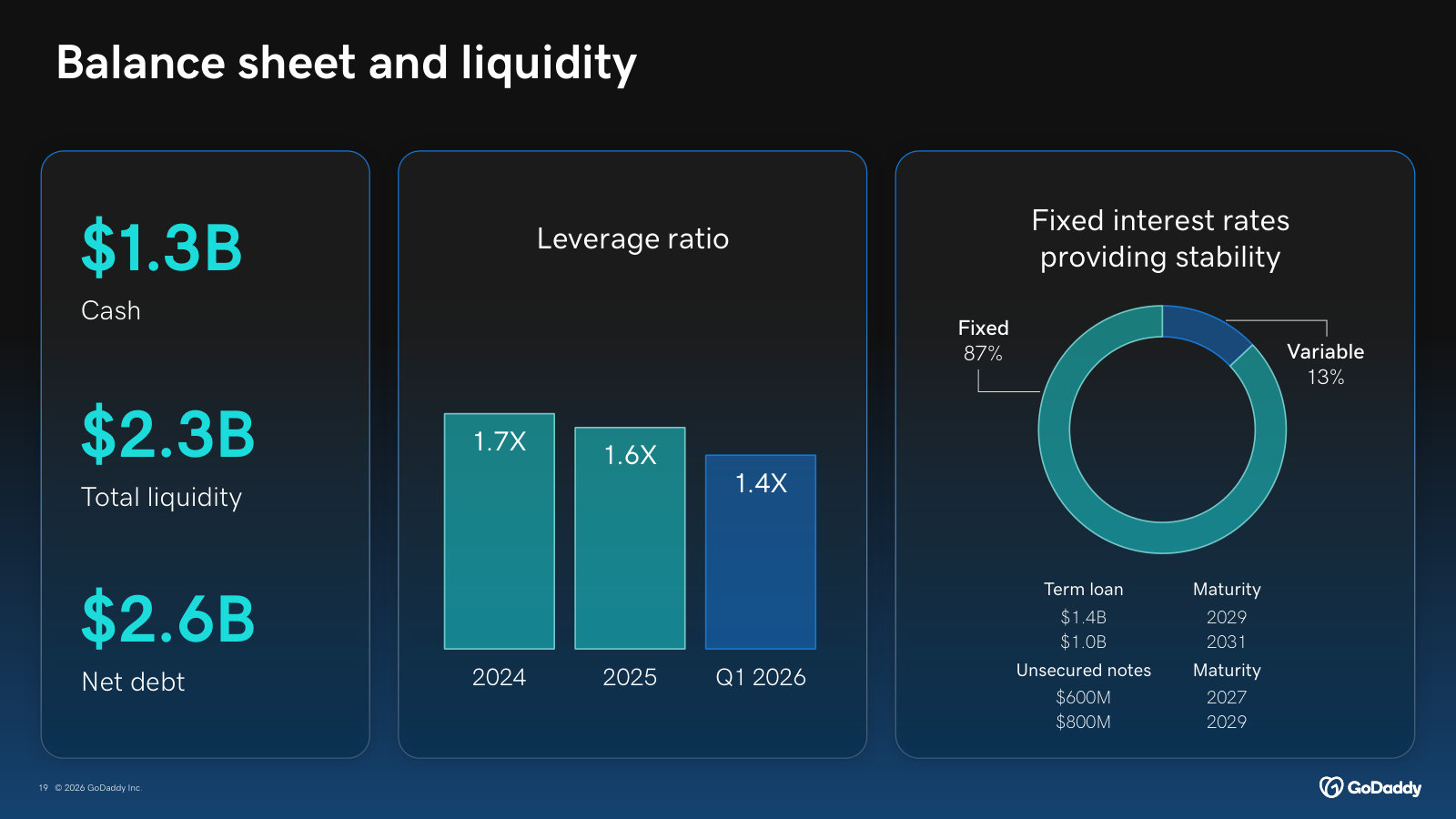

The balance sheet is where a cautious reader should slow down. GoDaddy carries $3.78 billion of long-term debt against $1.08 billion of cash, and years of buybacks have left total stockholders' equity at just $215 million and an accumulated deficit of $2.79 billion — with $3.63 billion of goodwill on the books, tangible equity is deeply negative [20]. That looks alarming in isolation. Set against the cash engine, it is more manageable than it appears: net leverage was 1.6x trailing EBITDA at year-end and 1.4x by the first quarter of 2026, interest expense of $151 million is covered about ten times by operating cash flow, and the company had $999 million available under its revolver and was in compliance with all covenants [21]. The negative book equity is a legacy of the buyback policy and the 2011 leveraged buyout, not a sign of distress — but it does mean the equity has no accounting cushion, and the model depends on cash flow staying strong.

From market darling to fallen star

GoDaddy came public in April 2015 at $20.00 a share, the exit vehicle for a 2011 leveraged buyout led by KKR and Silver Lake [22]. Founder Bob Parsons had already handed operating control to the sponsors; today the company is run by a professional management team under CEO Aman Bhutani, with none of the founder ownership the term "GoDaddy" might imply [23]. The stock compounded quietly for years, then ran hard through 2024 on enthusiasm for margin expansion and AI-driven small-business tools, peaking at $214 in late January 2025. It has since given back most of that move.

Source: NYSE daily price history; 2026 point is the July 10, 2026 close. Intra-year peak of $214.35 reached January 28, 2025 (market data, as reported).

What the fall did to the valuation matters more than the fall itself. At about $89, and on consensus estimates, GoDaddy trades at roughly 12.5 times expected FY2026 earnings of $7.11 and under 10 times the FY2027 estimate of $8.97; against guided FY2026 free cash flow of about $1.8 billion, the enterprise is valued at roughly 8 times [24]. The sell-side has cooled to match: of sixteen analysts, none rate the stock a sell, but eight now sit at hold, and the median price target of $100 implies only modest upside. This is no longer a high-flyer's multiple; it is the multiple of a business the market has decided will grow slowly.

Whether slowly is the right word is the open question. Management guides FY2026 to about 6% revenue growth — Applications and Commerce in the low double digits, Core in the low single digits — while reaffirming a free-cash-flow "North Star" of a 20%-plus compound growth rate, a gap it expects to bridge with margin expansion and a shrinking share count rather than faster sales [25]. Part of the 2026 deceleration is self-inflicted and arguably temporary — a shift to shorter contract terms, the loss of a .CO registry contract, and the exclusion of lumpy aftermarket sales together cost about two points of growth — but part of it is the underlying reality of a maturing core [26].

The question this report answers

GoDaddy is a highly cash-generative, asset-light franchise that has fallen roughly 60% from its peak to a mid-single-digit-growth valuation, run by professional managers who return all of their cash to shareholders and shrink the share count aggressively. The question the rest of this report exists to answer is whether that is a durable compounder handed to patient buyers at a value price because growth merely cooled to the mid-single digits — or a maturing domains-and-hosting business whose growth increasingly depends on charging a flat-to-shrinking base of customers more each year, on a balance sheet that carries $3.8 billion of debt and almost no book equity. Every chapter that follows tests one side of that question: how durable the pricing-and-attach engine really is, what the last three years of financials and the forward estimates actually show, who owns and runs the company and how they are paid, how much of the fall reflects real deterioration versus sentiment, and where the margin of safety is — or is not.

Financials and Estimates

Over FY2023–FY2025 GoDaddy's operating income roughly doubled and free cash flow rose 57%, yet reported net income fell — a divergence created almost entirely by income-tax accounting, not by any deterioration in the business [1]. The forward view is a business consensus expects to grow revenue around 6% while compounding earnings per share in the mid-teens to mid-twenties, on trivial cash taxes [2].

FY2025 Revenue ($M)

Operating Income ($M)

Free Cash Flow ($M)

Cash Taxes Paid ($M)

Source: FY2025 Annual Report (Form 10-K) — Statements of Operations [3], Cash Flows [4], Income Taxes [5].

The three-year income statement

Revenue rose from $4,254.1M in FY2023 to $4,951.1M in FY2025, an 8.3% gain in the most recent year and a 7.9% annualized pace over the two years [6]. What stands out is not the top line but what happened below it: operating income climbed from $547.4M to $1,127.3M, and the operating margin expanded from 12.9% to 22.8% [7].

Source: FY2025 Annual Report (Form 10-K), MD&A — Results of Operations [8].

The margin gain is a story of fixed-cost leverage rather than cost-cutting. Total costs and operating expenses rose only 3.2% over the two years — from $3,706.7M to $3,823.8M — while revenue rose 16.4% [9]. Put differently, about 83 cents of every incremental revenue dollar fell through to operating income. Part of that is a genuine wind-down of past-cycle charges: restructuring dropped from $90.8M to $11.1M and depreciation and amortization fell from $171.3M to $116.6M as acquired intangibles ran off [10]. The rest is scale: technology, marketing and customer-care lines were roughly flat in dollars against a revenue base that grew by nearly $700M.

Reported earnings fell while pretax profit grew

Below operating income, the picture inverts. Reported net income attributable to GoDaddy declined from $1,374.8M in FY2023 to $936.9M in FY2024 to $875.0M in FY2025; basic earnings per share fell from $9.27 to $6.34 [11]. A screen sorting on EPS growth would flag GoDaddy as a company in decline. It is not. Income before income taxes moved the other way — from $403.8M to $1,020.0M, a 2.5-fold increase [12].

Source: FY2025 Annual Report (Form 10-K), Consolidated Statements of Operations [13].

The entire divergence sits on the tax line. FY2023 carried an income-tax benefit of $971.8M and FY2024 a further benefit of $171.5M, while FY2025 recorded a normal tax provision of $145.0M at a 14.2% effective rate [14]. Those prior-year benefits came from recognizing deferred tax assets — GoDaddy stopped maintaining a valuation allowance against most of its U.S. federal and state deferred tax assets, and a legal-entity restructuring added more — which flattered FY2023–FY2024 net income by hundreds of millions of non-recurring, non-operating dollars [15]. Measured on pretax profit, FY2025 is by far the strongest of the three years; measured on reported EPS, it looks the weakest.

The three-year decline in GoDaddy's reported net income and EPS is an artifact of income-tax accounting. Pretax income rose from $403.8M to $1,020.0M while prior-year tax benefits of roughly $1.1 billion combined unwound to a normal 14.2% tax rate. Operating and cash performance improved every year.

Cash taxes and the NOL shield

The tax swing that depressed reported earnings has a mirror image in cash: GoDaddy pays almost nothing in cash tax. Cash paid for income taxes was $16.5M in FY2025, $19.1M in FY2024 and $10.6M in FY2023 — against pretax income that reached $1,020.0M [16]. The FY2025 book provision of $145.0M is therefore largely deferred, not paid: the cash-flow statement adds back $157.4M of deferred taxes, having subtracted a $993.2M deferred benefit back in FY2023 [17]. The shield is durable: at year-end FY2025 GoDaddy held $5,332.3M of gross net operating losses and tax credits, of which only about $2.1 billion sits behind a valuation allowance, with the balance available to offset future taxable income [18].

That is why free cash flow runs ahead of net income. Operating cash flow rose from $1,047.6M to $1,599.4M, and with capital spending of just $23.9M — under 0.5% of revenue — free cash flow reached $1,575.5M, 1.8 times reported net income [19].

Source: FY2025 Annual Report (Form 10-K), MD&A — Cash Flows [20] and Consolidated Statements of Cash Flows [21].

One honest offset belongs here. Free cash flow is struck after adding back $317.8M of equity-based compensation, up from $296.3M in FY2023 — a real cost borne by shareholders through dilution rather than cash [22]. Charging that compensation against FCF would cut FY2025 free cash flow to roughly $1.26 billion. The buyback program that consumed 100% of reported FCF in FY2025 is, in part, spending cash to hold the share count against that ongoing issuance.

Where the growth comes from

The two reporting segments are moving at different speeds, and the mix is shifting toward the higher-margin one. Applications & Commerce — website building, commerce and payments, and third-party productivity such as Microsoft 365 — grew revenue 14.3% in FY2025 to $1,889.0M and carries a 45% segment-EBITDA margin [23]. Core Platform grew 4.9% to $3,062.1M, but that number hides a split: domains revenue rose from $2,018.5M to $2,310.5M over two years while the remaining "other" Core line — legacy hosting and add-ons — fell from $805.2M to $751.6M as GoDaddy migrated customers off end-of-life products [24].

Source: FY2025 Annual Report (Form 10-K), Disaggregated Revenue [25].

Segment profitability improved on both sides. A&C segment EBITDA rose from $594.2M to $856.9M and Core from $816.4M to $1,010.3M; total segment EBITDA reached $1,867.2M against roughly $281M of unallocated corporate overhead [26]. The growth mix matters for the durable-versus-maturing question: the fast, high-margin part of the business (A&C, plus domains) is compounding at low-teens rates, while the slow-growth drag is a shrinking legacy tail — not the core franchise.

The forward view

Consensus frames the next two years as steady revenue with faster earnings. Analysts model revenue of about $5,242M in FY2026 and $5,549M in FY2027 — growth near 5.9% in each year — while consensus EPS rises from $6.22 in FY2025 to $7.11 in FY2026 and $8.97 in FY2027, gains of roughly 14% and 26%.

Source: consensus estimates (16 analysts for revenue, 12 for EPS); FY2025 actual per FY2025 Annual Report (Form 10-K) [27].

Management's own FY2026 guidance is consistent with that: revenue of $5.195–5.275 billion, about 6% growth at the midpoint, a normalized EBITDA margin above 33%, and free cash flow of roughly $1.8 billion at greater than 1:1 conversion, with a reaffirmed 20%-plus free-cash-flow-per-share compounding target [28]. The guide also absorbs just over 200 basis points of self-inflicted and one-off revenue drag in FY2026 — the loss of the .CO registry contract and the exclusion of high-value aftermarket transactions account for about two-thirds, and a go-to-market shift toward shorter initial contract terms the remaining third [29].

The gap between ~6% revenue growth and mid-teens-to-mid-twenties EPS growth is the whole engine of the forward case: continued margin expansion plus a share count that management has shrunk about 33% since 2021 and continues to reduce. It rests on two assumptions worth watching. First, that the effective tax rate stays low — the 14.2% booked in FY2025 is helped by research credits and stock-compensation benefits, and a drift toward the low-20s statutory zone would trim GAAP EPS growth even as cash taxes stay shielded by NOLs into the back half of the decade [30]. Second, that revenue does not decelerate further — the ~6% pace is guided, not achieved, and the recent revision trend is modestly negative, with FY2026 and FY2027 EPS estimates edged down over the past month.

Source: consensus analyst recommendations, as reported.

The sell-side sits split, not bullish: 8 buy or strong-buy ratings against 8 holds and no sells, with a median price target of $100 and a mean near $112 against a share price of about $89 — a spread of high-$83 lows to a $190 high. The distribution reads as a market that accepts the cash-generation case but is unwilling to pay up for a mid-single-digit grower until the revenue line reaccelerates or the buyback-driven EPS math proves itself. For a business whose operating profit and cash flow have compounded through a period when its own reported earnings said otherwise, that reconciliation — clean cash and rising pretax profit against a cooling top line and a normalizing tax rate — is where the durable-compounder and the maturing-business readings meet.

Competitive Moat

GoDaddy's moat is real but narrow. It rests on domain scale — the world's largest registrar, roughly a fifth of all names, over 85% retention — which buys durable pricing power, now expressed as a deliberate choice to shed low-value customers and monetize a flat base harder. The same AI wave GoDaddy is monetizing through Airo is also the sharpest threat to the domain-and-website premise the moat is built on. The near-term advantage is defensible; its durability is contingent on that transition.

What the advantage actually is

Three things carry the moat, and each shows up in a number. First, scale and brand: GoDaddy manages roughly 81 million domains, about 21% of the ~387 million registered worldwide, and describes itself as the world's largest registrar "by far" [1] [2]. Second, switching costs: the domain is, in management's words, "the front door to our platform," and the identity, email, website and commerce products a customer attaches all hang off it — leaving means moving a registrar, migrating email, and rebuilding a site [3]. Third, a recurring, prepaid revenue base: 20.4 million customers renewing at over 85% retention [4].

Domains Under Mgmt (M)

Share of Global Names

Paying Customers (M)

Customer Retention

Source: FY2025 Annual Report (Form 10-K), Item 1 Business [5]; retention above 85% for FY2025.

None of this is execution dressed up as a moat. Scale in domains is structural — it is the accumulated inventory of a 30-year head start, and GoDaddy notes it has already survived "low-priced registrars, loss-leader strategies, free domains and disruptive technologies" over that span while remaining the leader [6]. The company itself names retention, pricing and bundling, and attach — not new-customer volume — as the primary drivers of growth [7].

Pricing power, exercised as a strategy

The clearest proof of pricing power is that GoDaddy is now choosing to run a smaller base on purpose. Management has said plainly it "will let lower-LTV customers go because our focus is on high-intent customers," and in Q1 2026 it removed a lower-value product line to tilt the mix toward customers who attach and renew [8] [9]. This is the mechanism behind the pattern established in the orientation chapter: customers and domains under management are roughly 3% lower than two years ago while ARPU has climbed from $203 to $242, up 10% in FY2025 alone [10]. A firm without pricing power cannot shrink its customer count and grow revenue at the same time.

The economics concentrate at the top of the base. Customers spending more than $500 a year grew 11%, now represent about 10% of the total base, carry higher second- and third-product attach, and — in management's phrase — have "near-perfect retention" [11].

The counter-fact sits in the same data, and it matters: this is not purely price on a captive base. A new one-year domain offer drove new registrations up 6% for independent and partner customers, and A&C revenue grew 12% on genuine attach adoption [12]. So the pricing engine is not simply squeezing renewals; some of the ARPU lift is customers buying more. The limitation is different, and structural: monetizing a flat-to-shrinking base is inherently self-capping. Pricing power that runs by pruning units eventually meets the base it is pruning.

A crowded field, and where GoDaddy sits in it

The market is, by GoDaddy's own description, "highly fragmented and competitive," and its FY2025 10-K names more than thirty rivals across its segments [13].

Source: FY2025 Annual Report (Form 10-K), Item 1 Competition [14].

The list is long, but no single rival matches GoDaddy on both scale and profitability in its core lane. The nearest listed pure-play DIY-website builder, Wix, earns roughly a 6% operating margin on about a third of GoDaddy's revenue; GoDaddy earns close to 23% (see the financials chapter) [15]. The full-stack analogues — IONOS in Europe, GMO in Asia — are profitable but a fraction of GoDaddy's size, and the commerce specialists (Shopify, BigCommerce) compete in a different, transaction-led lane. The point is not that GoDaddy is unassailable; it is that the competitive threat is fragmentation and price pressure at the margin, not displacement by a larger incumbent.

Sources: GoDaddy FY2025 10-K, MD&A [16]; Wix FY2024 results, per peer financial data (revenue $1,760.7M, operating income $100.1M). Peer set is auto-selected; Wix is the cleanest direct DIY-builder comparison.

One wrinkle in that field is worth naming: Microsoft appears on GoDaddy's own competitor list across both segments, yet GoDaddy also resells Microsoft 365 email as a core productivity product [17] [18]. Part of the attach economics runs on a product supplied by a company that also competes with it — a dependency rather than an owned advantage.

The AI edge cuts both ways

GoDaddy's answer to the durability question is AI, and it is genuinely two-sided. On offense, the domain funnel feeds an AI layer that rivals cannot easily replicate: management cites close to 2 billion customer data points collected daily, used to tune agents "down to the customer grain" [19]. The early cohort evidence is real if small — customers routed through Airo show cumulative annual spend up in the high teens and second-product attach roughly 30% faster than non-Airo cohorts [20]. GoDaddy has also launched ANS, an open "trust layer" that registers AI agents under the domain system — an attempt to make domains the identity anchor for autonomous agents, extending the franchise into an agentic internet [21].

The threat is the mirror image, and GoDaddy states it in its own risk factors: the "widespread acceptance of any alternative system, such as mobile applications, AI-powered products and tools or closed networks, could eliminate the need to register a domain name or to establish an online presence" [22]. If customers increasingly reach the internet through AI platforms and closed ecosystems, demand for the builders, hosting and domains at the base of the moat could fall. The front door of the franchise is precisely what an agent-mediated internet could route around. ANS is GoDaddy's wager that domains remain the trust layer even then; it is a plausible bet, not yet a proven one — agents have only been registrable since late 2025 [23].

The read, and what would change it

On the moat playbook's scale, this is a narrow moat: durable and cash-generative today, defended by scale, brand and switching costs that show up in retention and pricing, but bounded on two sides — a base it is choosing to shrink, and a technology shift it does not control. It is not a wide moat, because the advantage defends and monetizes rather than compounds units; it is not absent, because the pricing evidence is unambiguous.

Three things would move the read. If domain units — primary registrations and total domains under management — stop declining and turn up as the high-intent pruning finishes, the "self-capping" concern weakens and the moat looks wider. If ARPU growth outruns the value delivered and retention slips below the mid-80s, the pricing engine is nearer its ceiling than it looks. And the decisive one over the next few years is whether Airo.ai and ANS add customers and attach rather than merely defend them — the difference between the AI transition extending the franchise and quietly hollowing out its front door. The moat's competitive durability is the load-bearing assumption behind the growth and margin trajectory the earlier chapters mapped; it is real, but it is contingent.

Ownership and Incentives

GoDaddy is not founder-run, and no insider owns a meaningful slice of it. All twelve directors and executive officers together hold 1,238,337 shares — under 1% of the company — and over the two years to July 2026 insiders filed 113 open-market sales worth about $57 million and not a single open-market purchase [1]. What alignment exists runs through pay, not ownership: roughly 90% of the CEO's package is equity, and its realized value swings hard with the stock. For a reader who prizes skin in the game, that is a real mark with genuine offsets.

No founder, no sponsor, no insider block

GoDaddy passed through every stage that usually leaves a large aligned holder and kept none of them. Founder Bob Parsons sold control to a KKR / Silver Lake / TCV buyout in 2011; the sponsors exited after the 2015 IPO; Parsons' own vehicle, YAM Special Holdings, last showed above 5% in 2018. The last sponsor-linked director, Silver Lake's Lee Wittlinger, sat on the board from its 2014 formation until his term lapsed around 2023 [2]. What is left is an ordinary institutional float — Vanguard at 14.3% and BlackRock at 10.7% are the only holders above 5% — and an insider group that owns under 1% [3].

The insider stake has drifted up as equity grants accumulate, but off a base so small the direction barely matters. The CEO's holding roughly doubled across four proxy cycles and still sits near half a percent.

All directors and officers as a group vs CEO Aman Bhutani, share counts per each year's beneficial-ownership table; percentages derived against shares outstanding disclosed in the same filing. Sources: 2022 Proxy [4]; 2023 Proxy [5]; 2024 Proxy [6]; 2026 Proxy [7].

At roughly $89 a share, CEO Aman Bhutani's 734,091 shares are worth about $65 million and the entire insider group about $110 million — real money to the individuals, but rounding error against an $11.8 billion market value [8]. About 319,000 of Bhutani's shares are awards settling within 60 days rather than stock he has held [9].

The trading tape reads one direction

The sharpest ownership signal is the flow, not the stock. Every insider transaction of the last two years was a disposal.

Insider Sales (2yr)

Open-Market Buys (2yr)

Sale Filings

Insider Ownership